Editor’s note: As GITEX Africa opens in Marrakech this week with data centre investment announcements expected, BETAR.africa looks at the structural constraints on African AI infrastructure.

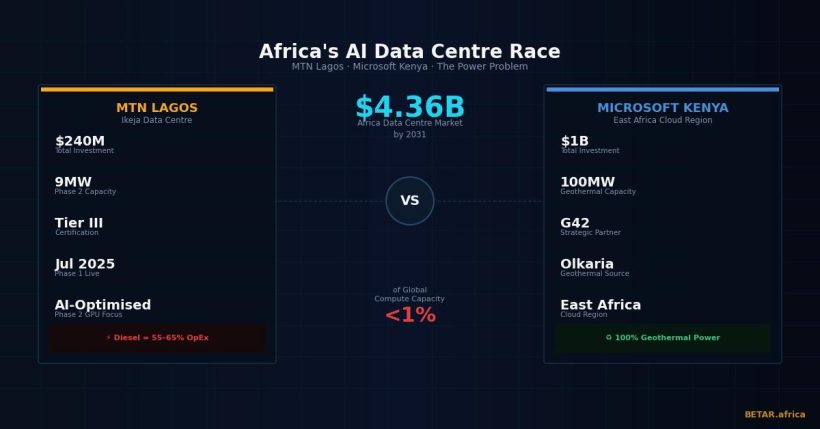

Africa is experiencing its first serious AI data centre investment wave. MTN has committed $240 million to an AI-optimised facility in Lagos. Microsoft and G42 are spending $1 billion on a geothermal-powered campus in Kenya. The African continent’s data centre market is forecast to grow from $1.94 billion in 2025 to $4.36 billion by 2031. The investment is real. So is the problem that threatens to constrain how much of it actually converts into usable AI infrastructure: power.

The challenge is not unique to Africa, but it is sharper here than anywhere else. AI workloads are extraordinarily energy-intensive — an inference query demands roughly ten times the power of a standard web request, and training a large model requires orders of magnitude more. Building data centres that can absorb that load at scale requires reliable, affordable, ideally renewable electricity. For most of sub-Saharan Africa, that electricity does not exist in the volumes required, or arrives at a price that renders AI infrastructure commercially marginal.

The Lagos Bet: MTN’s $240M Wager on Diesel and Demand

The MTN Sifiso Dabengwa Data Centre in Ikeja, Lagos, opened Phase 1 in July 2025. The facility is rated Tier III for concurrent maintainability — meaning it can sustain maintenance operations without shutting down — and delivers 4.5 megawatts of IT load capacity. Phase 2, scheduled for the second half of 2026, will expand capacity to 9 megawatts and introduce AI-optimised GPU infrastructure, bringing the total investment to $240 million.

The Phase 2 pivot toward AI is significant. Most African data centres have been built for enterprise IT workloads — storage, databases, business applications. MTN is making a deliberate bet that African AI demand, particularly from financial services, telecoms, and the growing Nigerian tech sector, will generate sufficient GPU utilisation to justify the infrastructure cost. The commercial logic is defensible. The energy constraint is the variable that could make or break it.

Nigeria’s grid remains among the most unreliable in the world. The data centre industry’s standard response is diesel generation — and Lagos-based facilities run diesel at a share of operating expenditure that would be considered extraordinary anywhere else. Industry estimates, validated by facility operators and publicly available energy audits, place diesel’s contribution to total opex at Lagos-class facilities between 55 and 65 per cent. The equivalent figure for comparable facilities in mature markets is 35 to 45 per cent. The delta is not a rounding error. It is a structural cost disadvantage that applies to every hour of compute the facility delivers, and it compounds as AI workloads — with their higher power draw and lower tolerance for downtime — replace the standard enterprise workloads the facility was originally designed to serve.

The MTN facility is not unique in this predicament. It is simply the most visible current example of a problem that applies to data centre investment across Nigeria: the energy infrastructure that makes AI-grade compute commercially viable has not been built yet, and no credible timeline exists for when it will be.

The Kenya Gamble: Microsoft’s Geothermal Logic

The Microsoft and G42 Kenya investment tells a structurally different story. The two companies — Microsoft providing enterprise cloud credibility, G42 providing Abu Dhabi sovereign capital and existing African infrastructure relationships — have committed $1 billion to a data centre campus in Kenya, anchored by a 100-megawatt geothermal power allocation from KenGen’s Olkaria facility in the Rift Valley. The project will host the Azure East Africa Cloud Region, Microsoft’s first African cloud region north of South Africa, with an expected launch around mid-2026.

The geothermal anchor is the critical variable. Kenya generates over 90 per cent of its electricity from renewable sources, with geothermal — baseload, stable, available regardless of rainfall or sunlight — contributing roughly 45 per cent of the national grid. The Olkaria field, where the Microsoft-G42 facility’s power will originate, currently generates approximately 840 megawatts and KenGen has outlined expansion capacity to over 1,700 megawatts. Diesel, which functions as the primary backup and often primary source for Lagos data centres, is not in the operational vocabulary of the Kenya project.

The result is a cost structure that simply cannot be replicated in West Africa on current timelines. A Lagos facility paying diesel-inflated power prices at 55–65 per cent of opex faces a fundamentally different economics than a Nairobi facility connected to geothermal baseload. The gap in energy cost per megawatt-hour — rough industry estimates place Kenyan grid power for industrial users at $0.06–0.09/kWh versus diesel generation in Lagos at $0.18–0.25/kWh — is the single largest factor differentiating the economics of AI infrastructure across the two corridors.

G42’s involvement is also structurally notable beyond the capital it brings. The company’s model — deploying infrastructure rapidly in markets where it has government relationships, then filling it with Microsoft Azure services and AI workloads — has become a template that other Gulf sovereign-backed infrastructure players are watching closely. If the Kenya project delivers, it validates a capital structure for African AI infrastructure that does not depend on development finance institutions or long concessional timelines.

The Continental Picture: Investment Real, Share Declining

Africa’s total active data centre capacity stood at approximately 360 megawatts as of early 2026, according to the Africa Data Centre Association, representing roughly 0.6 per cent of global installed capacity. The pipeline — projects under construction or with committed funding — adds approximately 1.2 gigawatts of planned capacity. That pipeline is genuine. The numbers behind it are large enough to represent a meaningful expansion of continental infrastructure.

The concern is the denominator. Global hyperscaler capital expenditure is expected to exceed $600 billion in 2026, with Microsoft, Google, Amazon, and Meta collectively accounting for the majority of that spend. Against that scale of investment in the US, Europe, and Asia Pacific, Africa’s pipeline — even at 1.2 gigawatts — is unlikely to shift the continent’s share of global compute capacity. Africa is not falling behind; it is building. But the gap between African AI infrastructure and global AI infrastructure is widening in absolute terms even as the continent invests more than it ever has in nominal figures.

Google’s Johannesburg cloud region, which launched in January 2024, represents a third model alongside the MTN Lagos and Microsoft Kenya approaches — a hyperscaler investing directly in continental infrastructure, rather than through a local partner or JV structure. Google has also invested in the Umoja subsea cable, which connects the East African coast to Europe and provides the high-bandwidth international connectivity that modern AI data centres require for data transfer and model delivery. But Johannesburg faces the same South African energy question that MTN faces in Lagos: Eskom’s grid instability, though improving after years of load-shedding, is still not the foundation on which power-intensive AI infrastructure builds without risk mitigation cost.

The Constraint That Matters

The argument that Africa cannot build competitive AI infrastructure because it lacks capital has never fully held up. The MTN commitment, the Microsoft-G42 billion-dollar investment, and the broader $4.36 billion market trajectory suggest that capital is available for proven infrastructure cases. What the Kenya-Nigeria comparison makes concrete is that capital is necessary but not sufficient. Power — stable, affordable, high-volume, renewable power — is the binding constraint that determines whether the investment converts into useful compute or into diesel-subsidised infrastructure operating at cost disadvantage.

That constraint is not permanent. Nigeria has the solar resource, and increasingly the capital interest, to build utility-scale renewable generation. Kenya’s geothermal advantage is replicable, in different forms, across East Africa’s rift corridor. Ethiopia’s hydropower infrastructure, once grid connectivity reaches commercial maturity, could anchor similar investments. The constraint that will determine how quickly the AI infrastructure gap narrows is not capital. It is power — and specifically, the speed at which continental energy policy and investment produces the stable, affordable electricity that AI-grade data centres require as a precondition, not a feature.

Africa’s data centre investment wave is real. The continent’s power problem is equally real. The projects that succeed will be the ones built where those two realities have been squared.

Africa AI Data Centre Investment: Key Projects Comparison, 2025–2026

| Project | Location | Investment | IT Capacity | Timeline | Power Source | Power Cost Exposure |

|---|---|---|---|---|---|---|

| MTN Sifiso Dabengwa DC (Phase 1) | Ikeja, Lagos, Nigeria | Part of $240M total | 4.5MW | Operational July 2025 | Grid + diesel backup | High (55–65% opex diesel) |

| MTN Sifiso Dabengwa DC (Phase 2, AI GPU) | Ikeja, Lagos, Nigeria | $240M total | 9MW (AI-optimised) | H2 2026 | Grid + diesel backup | High (structural) |

| Microsoft + G42 East Africa Cloud Region | Nairobi, Kenya | $1B | 100MW (geothermal-anchored) | ~Mid-2026 | KenGen geothermal (Olkaria) | Low (renewable baseload) |

| Google Johannesburg Cloud Region | Johannesburg, South Africa | Undisclosed | Not confirmed at scale | Live Jan 2024 | Eskom grid + renewables | Medium (improving grid stability) |

| Cassava / Liquid Intelligent Technologies (GPU-as-a-Service) | SA, Nigeria, Kenya, Egypt, Morocco | Undisclosed | Distributed (GPUaaS) | Operational 2025 | Mixed (market-dependent) | Variable by location |

Sources: MTN Group investor presentations; Microsoft and G42 joint announcement; Africa Data Centre Association 2026 capacity report; KenGen annual report; Cassava Technologies announcement. Investment figures as reported by companies. Capacity figures as at Q1 2026 or announced targets.

For analysis of AI developer compute costs and the cloud pricing gap facing African AI builders, see our companion piece: Africa AI Compute Gap: The 3× Premium African Developers Pay for GPU Access.