Kenya’s telecoms regulator has released quality-of-service assessment data that puts Telkom Kenya on a collision course with enforcement action — and raises a harder question the industry has been quietly deferring: is the country’s third operator viable enough to survive independently?

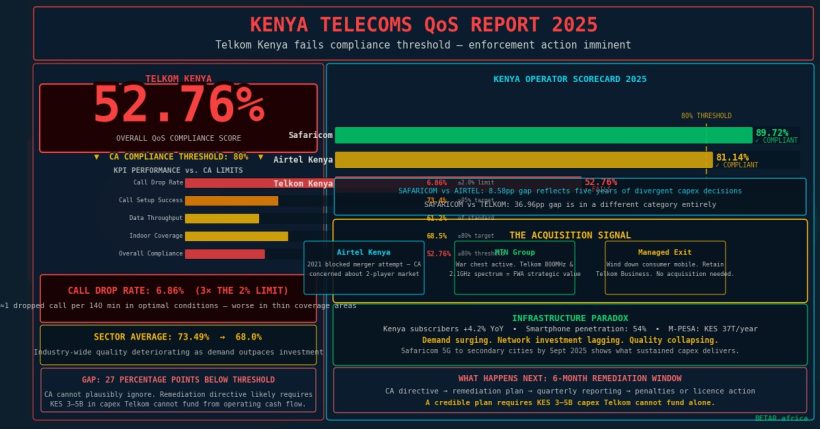

The Communications Authority of Kenya’s annual QoS assessment for 2024–2025, published on 1 April 2026, records Telkom Kenya’s overall compliance score at 52.76%. The CA’s compliance threshold is 80%. At 52.76%, Telkom is not only below the threshold — it is the worst-performing licensed operator in Kenya by a margin that the CA cannot plausibly ignore without signalling that its enforcement posture is discretionary.

The sector-wide picture is also deteriorating. The industry average compliance score fell from 73.49% in the 2023–2024 assessment to 68% in the latest cycle. Kenya is getting faster smartphones, growing mobile money volumes, and rising digital services consumption. Its underlying network quality is moving in the opposite direction.

What the numbers show

The CA’s assessment benchmarks operators against a standard set of key performance indicators: call setup success rate, call drop rate, indoor and outdoor coverage, data throughput, and latency. Telkom Kenya failed to meet the threshold across the majority of KPIs measured.

The call drop rate figure is the most operationally significant. Kenya’s CA sets a maximum permissible call drop rate of 2%. Telkom Kenya recorded a call drop rate of 6.86% — more than three times the limit. For a subscriber making ten calls per day, that translates to approximately one dropped call every 140 minutes of talk time under optimal conditions. In practice, in the areas where Telkom’s coverage is thinnest, the experience is worse.

Safaricom scored 89.72% overall, leading across all primary KPIs. Airtel Kenya recorded 81.14% — barely above the compliance threshold, and a figure that warrants its own scrutiny. That Airtel Kenya is nominally compliant while scoring 81% should not obscure the fact that it is thirteen percentage points below Safaricom on the same assessment. The gap between Africa’s most sophisticated mobile money operator and its main challenger is measurable, documented, and growing.

Telkom Kenya’s 52.76% is in a different category entirely.

The enforcement question

The CA has several tools available. These range from formal directives requiring remediation plans — with quarterly reporting obligations — to financial penalties and, at the extreme end of the scale, licence suspension. The CA’s enforcement framework does not mandate suspension at any particular compliance floor, but a score 27 percentage points below the threshold gives the regulator ample justification to impose structured remediation requirements with financial consequences for non-compliance.

Telkom Kenya’s response to the assessment has not been publicly detailed at time of publication. The operator has been in a quiet infrastructure rationalisation phase since 2024, when it began negotiations around its tower assets held through its ATC Kenya partnership. The tower negotiations are relevant here: Telkom’s QoS performance is partly a function of its network investment posture, and a company actively managing down infrastructure costs is not in a position to simultaneously pursue the capex programme that meaningful QoS improvement requires.

The CA is aware of this dynamic. Regulatory enforcement that demands investment from an operator whose balance sheet cannot support that investment without triggering a restructuring event is not enforcement — it is a mechanism for forcing a decision that the market has been deferring.

The acquisition signal

Telkom Kenya has been the subject of acquisition speculation for three years. The 2021 Airtel Kenya merger attempt — blocked by the CA on competition grounds — remains the most serious acquisition attempt on record. The competitive rationale at the time was straightforward: Airtel Kenya acquiring Telkom’s subscriber base and spectrum would create a credible #2 operator capable of sustaining pressure on Safaricom’s dominant position.

The CA’s competition concern in 2021 was that a two-operator market would reduce competitive pressure on pricing. That concern has not disappeared. But the context has shifted. A Telkom Kenya that is structurally non-compliant, under enforcement action, and unable to fund the capex required for remediation is a different regulatory consideration than a Telkom that was financially marginal but operationally functional.

There are potential acquirers beyond Airtel Kenya. MTN Group, which has publicly signalled acquisition appetite in Eastern and Southern Africa as part of its war chest strategy, would find Telkom Kenya’s spectrum holdings — particularly in the 800MHz and 2.1GHz bands — strategically valuable for its fixed wireless access push. Telkom Kenya holds spectrum that would materially accelerate FWA deployment in Nairobi’s peri-urban belt, where MTN currently has no presence.

A third possibility is a managed exit: Telkom Kenya winds down the consumer mobile business, sells or transfers spectrum to the CA for refarming, and retains its enterprise and fixed broadband operations — the Telkom Business unit, which has historically been the operator’s most stable revenue line. This outcome would reduce the licensed operators in Kenya’s mobile market from three to two without a formal acquisition, and without the competition review that an Airtel or MTN acquisition would trigger.

The infrastructure paradox

The QoS deterioration documented in the CA’s assessment does not reflect a market in decline. Kenya’s mobile subscriber base grew 4.2% year-on-year to 2024. Smartphone penetration has reached 54% nationally and continues to grow, driven by device financing schemes and sub-$100 entry-level 4G handsets. Mobile data consumption volumes are rising. M-PESA processed KES 37 trillion in the 12 months to June 2025.

Rising usage on a network that is not expanding at a commensurate rate produces exactly the quality degradation the CA’s assessment documents. The decline in the sector average from 73.49% to 68% is not an anomaly — it is the predictable consequence of demand outpacing investment in a market where two of three operators are capital-constrained.

Safaricom’s 89.72% score demonstrates that QoS compliance at scale is achievable in Kenya. The company’s infrastructure investment programme — including the September 2025 completion of its 5G expansion to secondary cities — shows what sustained capex commitment produces in a market with Kenya’s geographic and demographic complexity. The gap between Safaricom and the field is not a regulatory artefact. It reflects five years of divergent investment decisions.

What happens next

The CA’s standard procedure following a QoS assessment is to issue compliance improvement directives to operators scoring below threshold, with a six-month remediation window and quarterly reporting requirements. For Telkom Kenya, the practical question is whether a remediation plan submitted to the CA will be credible given the operator’s financial position.

A remediation plan that requires KES 3–5 billion in new network investment — the order of magnitude required to close a 27-percentage-point compliance gap — is not a plan Telkom Kenya can fund from operating cash flow. It requires either debt financing, equity injection, or a strategic partner. Each of those paths implies a change in ownership structure that the 2026 QoS enforcement process may effectively force into the open.

Kenya’s mobile market is heading toward a structural decision that the CA’s assessment data has now made unavoidable. The regulator did not create the problem. It has documented it with sufficient precision that deferral is no longer credible.

BETAR.africa sought comment from Telkom Kenya on the QoS assessment results and its remediation plan. A response was not received by publication time. The CA Kenya assessment figures cited are drawn from the publicly released 2024–2025 annual report.