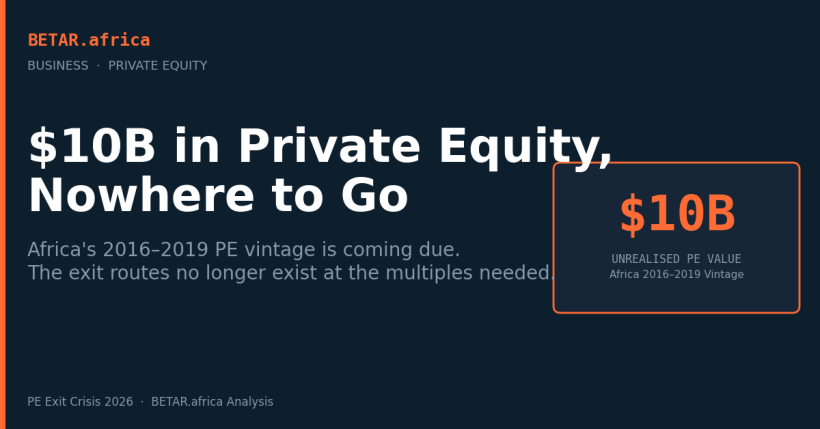

Africa PE Exit Crisis 2026: $10B in Private Equity, Nowhere to Go

The vintage years of 2016–2019 are coming due. African PE managers hold an estimated $10 billion in unrealised value — and the exit routes they underwrote are not available at the multiples they need.

The vintage years of 2016, 2017, and 2018 were good times to be an African private equity manager. The continent’s growth story was intact, DFI capital was abundant, and the global investors arriving in Lagos and Nairobi wanted exposure to consumer middle-class expansion, financial inclusion, and infrastructure build-out. Funds raised, capital deployed, portfolio companies acquired.

Eight years later, the exits have not arrived. The companies built during that period — consumer-facing businesses, agri-processing platforms, financial services plays, logistics consolidators — are still largely PE-owned. The managers who raised on seven-year fund timelines are now three to five years past their original horizon. And the exit routes that were assumed to exist — IPOs, strategic sales, regional acquirers — are either shallow, closed, or simply not transacting at valuations that work.

The result is an industry-wide holding pattern that AVCA estimates now covers more than $10 billion in unrealised portfolio value. That number is not a failure of African business fundamentals. It is a failure of market architecture.

The Age Problem

Private equity funds operate on a mechanical logic: raise capital from limited partners, deploy over three to four years, grow portfolio companies, exit within seven to ten years, return capital. The discipline of the fund structure is also its constraint — it creates hard deadlines that the market does not always accommodate.

African PE funds raised between 2016 and 2019 — the period AVCA identifies as the continent’s most active primary fundraising window — are now approaching or past the standard hold-period boundary. The average hold period for African PE assets has extended from 5.8 years in 2018 to an estimated 7.2 years in 2025, according to AVCA’s most recent data. That extension is not the result of managers choosing to hold longer. It is the result of exit markets not absorbing supply.

The fund vintage problem is concentrated in mid-market deals — companies acquired for enterprise values of $50 million to $250 million, typically in healthcare, consumer goods, financial services, and agro-processing. These are too large for the seed and Series A acquisition market, too small for the handful of global strategic buyers active in Africa, and too operationally specific for the multinational corporates that have been African PE’s most reliable exit counterparty.

Helios Investment Partners, the largest Africa-focused PE manager by AUM at approximately $3 billion under management, has been navigating this problem since its third fund (2015 vintage) entered its extension period. DPI — Development Partners International — whose Africa Fund III closed in 2019 at $900 million, is increasingly focused on secondary processes as primary exit routes prove thin. African Capital Alliance, with its fourth fund (2018 vintage), has deployed capital but faces a Nigerian operating environment that has dramatically altered the exit math on naira-denominated businesses.

Exit Route by Route: What Works in 2026

IPOs: The least viable route at scale.

BETAR’s analysis of African exchange activity through Q1 2026 finds fewer than five significant new listings on the NSE, JSE, and GXG combined since the start of 2025. The companies most plausibly approaching IPO readiness — Moniepoint, Wave, Breadfast — are either not at public-market scale, not ready to tolerate the disclosure requirements, or deliberately waiting for a more favourable market window. None of the major PE-held mid-market industrials or consumer companies are in the IPO pipeline.

The NSE has announced structural reforms to attract tech listings. The JSE remains liquid but PE-exit-friendly only for companies with R1 billion+ revenue and institutional-grade governance. For a Ghanaian healthcare company or a Nigerian fast-food chain held since 2017, the JSE is not a plausible exit vehicle.

African exchanges are, with limited exceptions, an exit route for the future rather than a mechanism for clearing the current backlog.

Strategic Sales: Available for exceptional assets; absent for most.

Strategic sales — selling a portfolio company to a global or regional corporate acquirer — have historically been African PE’s most reliable exit mechanism. The logic holds when multinational companies are expanding onto the continent, paying control premiums for market entry or consolidation. That logic held well from 2010 to 2018.

The current environment is different. Global M&A activity has contracted as high interest rates have raised the cost of acquisition financing. African-specific strategic buyers — the pan-African corporates with the balance sheet and geographic ambition to absorb PE-held assets — are few and deal-specific. Diageo, Heineken, and Tiger Brands have been active acquirers in their sectors, but they are not absorbing the broad mid-market backlog.

DPI’s most successful recent exit — its secondary sale of a stake in Moniepoint as part of that company’s 2024 Series C — represents the exception: a high-quality asset in a high-demand sector with well-understood metrics. The mid-market PE portfolio does not uniformly look like Moniepoint.

Secondary Fund-to-Fund Transactions: Growing but insufficient.

The secondary market — fund managers selling LP stakes or portfolio positions to secondary buyers — is the fastest-growing component of the African PE exit ecosystem in 2026. PROPARCO, the French development finance institution, completed three African PE secondary purchases in the past eighteen months. DEG, the German DFI, has been a consistent secondary buyer, and BII (formerly CDC) has been particularly active in facilitating secondaries that allow its co-investors to exit while BII maintains exposure.

Secondary transactions offer liquidity without requiring a public market or a strategic buyer. But they carry structural limitations: the universe of African PE secondary buyers is thin, concentrated in DFIs whose mandate requires them to prioritise development impact over return maximisation. Pure financial secondaries buyers — Lexington Partners, HarbourVest, Pantheon — have African exposure but transact selectively, favouring large fund stakes over individual asset purchases.

The secondary market is a genuine pressure valve. It is not yet a clearing mechanism for $10 billion in unrealised value.

Recapitalisations: A deferral, not an exit.

Dividend recapitalisations — borrowing against portfolio company assets to return capital to LPs without selling equity — are being explored by managers under LP distribution pressure. The venture debt and private credit expansion BETAR documented in Q1 2026 has created marginal capacity for recaps in more mature portfolio companies. But recap appetite depends on underlying business cashflows, and African mid-market companies carrying leverage in naira, cedi, or shilling face FX-adjusted debt service costs that limit how much additional debt the capital structures can absorb.

LP Pressure: The Clock That Cannot Stop

The extension of hold periods is an LP problem before it is a manager problem.

The major LPs in African PE funds are DFIs — BII, PROPARCO, DEG, IFC, Norfund — along with sovereign wealth funds (GPIF, GIC, Temasek in select vehicles), pension funds, and endowments. DFIs have development mandates that allow for patience capital. They can accommodate extensions that would trigger redemption pressure in a commercial fund. But DFI patience has limits: deployment committees, annual audits, and board governance structures all create accountability pressure.

Pension funds and endowments in the LP base face harder structural constraints. A pension fund with actuarial obligations cannot indefinitely defer distributions from a PE allocation. When distributions are delayed, re-up decisions suffer. The 2023 and 2024 vintages of African PE fundraises were notably harder than 2018 and 2019 — not because Africa’s fundamentals had deteriorated, but because LP sentiment on the exit track record had cooled.

Managers are responding with a mix of tactics. Secondary processes are being run quietly, positioning LPs for partial exits ahead of a full fund wind-down. GP-led restructurings — where a fund manager creates a continuation vehicle and offers LPs the choice to exit now or roll into the new structure — are being explored, though African PE’s small number of credible continuation vehicle buyers limits this option. NAV lending against portfolio positions has attracted interest, though African assets struggle to access this product at the rates available to US or European PE.

The LP clock cannot be suspended indefinitely. The market will clear — through secondaries, through below-expected strategic sales at reduced multiples, or through forced realisations when fund extension waivers expire. None of those outcomes are as good as the exit the 2016 and 2017 managers underwrote.

Winners, Losers, and What the Divergence Shows

The exit environment is not uniformly bad. The divergence between managers who have navigated well and those who have not illuminates what the African PE mid-market actually rewards.

Managers who have exited successfully hold assets with clear, FX-diversified revenue models — companies earning in dollars or dollar-linked currencies, or businesses with pricing power sufficient to sustain margins through currency pressure. They also concentrated in sectors with identifiable strategic buyers: healthcare (where global hospital groups and pharmaceutical distributors remain acquisitive), financial services (where the Moniepoint-style acquisition thesis is active), and logistics infrastructure (where pan-African industrial buyers have been transacting).

Managers who are stuck are disproportionately concentrated in consumer-facing naira and cedi-denominated businesses where devaluation has compressed USD-equivalent EBITDA and made exit multiples unattractive relative to entry. They hold assets acquired at 2019 or 2021 valuation expectations that the current macro environment does not support.

The asymmetry is instructive. African PE can generate exits — but the asset selection and currency positioning decisions made at entry are the dominant determinant of outcome, more than operational value creation during the hold period.

A Market at Inflection

The $10 billion holding pattern will not resolve in a single year. IPO markets will not open fast enough. Strategic buyers will not absorb the backlog quickly. The secondary market is growing but thin.

What will resolve the backlog, over three to five years, is a combination of forces already in motion: the accumulation of a generation of African PE managers with full cycle track records (including the difficult exits), the gradual deepening of secondary buyer capacity, and the emergence of the current cohort of tech-adjacent companies — Moniepoint, Onafriq, Wave — as acquirers in their own right, capable of absorbing the operational businesses that older PE funds built.

The 2016–2019 vintages will return capital to their LPs. Some of it will be below underwritten expectations. Some will surprise on the upside. The managers who navigate the current environment credibly — who run secondaries, communicate transparently with LPs, and find exits that are imperfect but executable — will raise the 2027 vintage. Those who do not will not.

Private equity in Africa is at an inflection point between a cycle built on macroeconomic growth assumptions and one that requires exit infrastructure to exist before the capital is committed. The infrastructure is being built. The 2016 vintage is paying the price for the construction delay.

Sources: AVCA African Private Capital Report 2025; BETAR Q1 2026 Funding Tracker; Partech Africa 2025 VC Report; DPI Africa Fund III investor materials; BII secondary transaction reporting 2025.

Related BETAR coverage: Africa’s Series A Desert: Local VCs Rising (BETA-566) | Venture Debt Fills the Africa Equity Gap (BETA-1028) | Africa IPO Pipeline 2026-2027 (BETA-1101) | Africa Q1 2026 Investor League Table (BETA-822)