Every Nollywood box office record, every Netflix Africa Original greenlight, every Ghanaian film festival circuit play begins with a producer raising money. The mechanisms through which African film productions are financed, budgeted, and brought to camera — and the economic value that accrues to each layer of that chain — remain one of the least-reported dimensions of the continent’s creative economy.

BETAR.africa has covered what streamers pay to license African content, what cinema exhibitors extract from ticket revenue, and what the intermediary layer takes from creators. What we have not mapped is the economics of production itself: how films get made, who bears the financial risk, and what Netflix’s $100 million-plus Africa investment commitment has done to cost structures on the ground.

The scale of the industry is significant: Nigeria’s National Film and Video Censors Board (NFVCB) registered approximately 2,599 films in 2022, down from a peak of over 2,900 in 2019 but still representing the second-largest film output by volume of any country in the world. The economics behind that volume — and the premium layer that has emerged atop it — are the subject of this report.

The Financing Stack

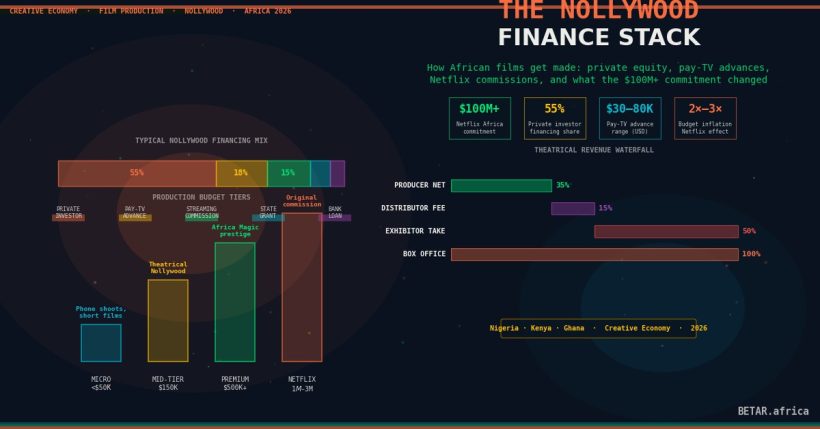

Nollywood’s production finance model has evolved significantly from the informal “Alaba market” system that dominated until the mid-2000s, when video distributors advanced production budgets in exchange for duplication rights. Today, the financing stack is more structured — though still highly fragmented by global standards.

Private equity and investor groups remain the dominant financing mechanism. Producer-directed investor circles — typically high-net-worth individuals drawn from business, diaspora, and entertainment communities — fund the majority of mid-tier Nollywood productions. These deals are typically structured as equity stakes or fixed-return loans with profit participation clauses once the film recoups.

“Most of my productions are still privately financed — a small group of investors who believe in the project and in me as a producer,” says Adaeze Nwosu, a Lagos-based independent producer whose credits include several mid-tier Nollywood features released on Amazon Prime Video and ShowMax. “The investor circle model works because we move fast. A bank loan takes three months; my investors can commit in three weeks. The trade-off is that they expect a return, and they expect it quickly.”

Advance licensing agreements with pay-TV operators have provided more predictable capital. Africa Magic (DSTV/MultiChoice) has historically offered pre-production advances against broadcast licensing rights, particularly for its premium Nollywood window. These advances — typically in the $30,000–$80,000 range for mid-tier productions — are non-recoupable against broadcast fees but may contain exclusivity windows that limit the producer’s ability to sell streaming rights simultaneously. The MultiChoice/Netflix competitive dynamic has tightened these arrangements in recent years, as producers increasingly weigh whether a pay-TV advance is worth foreclosing a potential streaming deal.

Institutional financing remains underdeveloped. Nigeria’s NEXIM Bank has operated film financing programmes, and the Bank of Industry’s creative industry intervention fund has provided loan facilities for eligible productions. However, take-up has been constrained.

“The gap is not appetite — it is documentation,” says Obinna Eze, Deputy Director of the Creative Industries Division at the Bank of Industry in Lagos. “Producers struggle to provide the bankable pre-sales or distribution agreements that allow us to treat the film as collateral. Until the distribution infrastructure matures — guaranteed minimum payments, verified box office data, structured streaming deal terms — formal lending at scale will remain difficult.” The Bank of Industry’s creative sector loan book grew 18% in 2024–25, but film production remains a small share relative to music and fashion.

The Kenya Film Commission provides production grants — ranging from approximately KES 500,000 to KES 5 million for eligible Kenyan productions — alongside co-production treaty facilitation, but its grant envelope is modest relative to the market’s overall financing needs.

Pre-sale streaming deals are the newest and most commercially significant financing mechanism for premium productions. Netflix and Prime Video both operate pre-production commissioning models in African markets for originals, delivering production capital against a full exclusive licensing arrangement. The key commercial distinction is between a commission (Netflix finances and owns the content, paying a work-for-hire fee to the production company) and a licence (Netflix acquires rights to an independently financed film after completion or at an advanced production stage). The economic implications differ materially: under a commission, the producer captures production margin but surrenders long-term rights; under a licence, the producer retains rights but bears the full financing risk.

Budget Economics

African film production spans a wide cost range, and the three broad tiers have distinct financing and commercial profiles.

Micro-budget productions (under $50,000) dominate by volume in Nollywood, where shooting efficiency on digital video, compressed shooting schedules, and established location networks allow producers to bring features to camera at costs that would be impossible in Western markets. Cast typically represents 30–40% of production spend; in micro-budget productions targeting fast-turnaround direct-to-streaming releases, cast costs are negotiated primarily in naira with upfront fees replacing backend participation.

Mid-tier productions ($50,000–$500,000) represent the commercial mainstream of premium Nollywood. Comparable data for Riverwood (Kenya) and Ghallywood (Ghana) at this tier is not systematically reported — producers in both markets declined to confirm specific budget ranges for this article — though industry practitioners indicate the upper end of Riverwood mid-tier sits below Nollywood equivalents, reflecting smaller domestic market scale.

Premium productions ($500,000–$3 million and above) are almost exclusively streamer-commissioned or co-produced with international partners. The budget composition at this tier begins to resemble international production norms: union-equivalent day rates, insurance requirements, international post-production pipelines, and formal completion guarantees.

The Netflix Effect on budget inflation is quantifiable by proxy. Productions that would have been budgeted at N100–150 million in 2020 are now budgeted at N300–500 million for equivalent scope — driven partly by naira depreciation inflating dollar-denominated costs, but also by rising crew day rates, cast fee expectations benchmarked against streamer-paid productions, and location costs in Lagos that have tracked real estate inflation. What a $1 million production budget buys in Nollywood today is materially less than what it bought in 2018.

The Netflix Effect

Netflix’s commitment of over $100 million to African originals since its 2016 continent-wide launch has restructured the economics of premium production in ways that extend beyond the productions it directly commissions.

The most direct effect has been on talent rates. Industry data compiled from production budget disclosures and producer interviews indicates that top-tier Nollywood actors who command N3–5 million per film in the independent market can negotiate N8–15 million for Netflix-commissioned productions, establishing a reference point that bleeds into non-Netflix negotiations. The same dynamic applies to experienced directors of photography and post-production supervisors. Crew day rates in premium Lagos productions have risen roughly 60–80% in dollar terms since 2021, driven primarily by benchmark-setting in the streamer-commissioned tier.

The commission-versus-licence distinction carries significant IP implications. “When Netflix commissions a production, they own it — globally, in perpetuity for the contract window,” says a senior content acquisitions executive at a major streaming platform operating in Sub-Saharan Africa, speaking on terms of commercial confidentiality. “For a producer, the question is: do you take the commission fee and certainty, or do you independently finance, retain the rights, and try to licence? The risk-return calculus depends entirely on your ability to raise independent production capital.” This executive confirmed that licence fees for completed African productions acquired by streaming platforms in 2024–25 ranged from $80,000 to $350,000 per title depending on language, production quality, and exclusivity scope.

Netflix’s commissioning structure creates a specific economic arrangement. For original commissions, Netflix typically pays the production company a fee that covers full production costs plus a margin — typically 10–20% of total budget, though this varies by negotiation. The production company owns no residual rights; Netflix holds the content. For African markets where the IP ownership economy is nascent, this model efficiently delivers production capital but creates no long-term asset value for the local production sector.

Post-Production Infrastructure

South Africa’s post-production industry is the continent’s most technically advanced, and it functions as a regional hub for productions across Southern and Eastern Africa. Cape Town and Johannesburg-based facilities offer grading, VFX, and sound design at internationally competitive rates, supported by the country’s DTIC film incentive which makes South African post-production spend eligible for a 25–35% rebate on qualifying local expenditure.

Nigeria’s post-production capacity has grown rapidly but remains constrained for complex work. Studios in Lekki and Victoria Island offer colour grading, sound mixing, and basic VFX for the local market, but complex visual effects — high-end compositing, period recreations — typically routes through South African or UK and US pipelines. The skill gap is commercially significant: it constrains the genres Nollywood can produce at competitive quality without inflating budgets beyond what the local market will support. Kenya’s post-production capacity, meanwhile, serves the Riverwood market and growing branded content sector, but Kenyan features requiring VFX-heavy production continue to route through South Africa.

Government Incentive Economics

South Africa’s DTIC film incentive offers the most commercially significant government subsidy on the continent. Productions meeting South African content criteria qualify for a rebate of 25–35% of qualifying South African Production Expenditure (QSAPE), paid post-production. The rebate has made South Africa a preferred destination for international productions seeking African locations — co-productions with US, UK, and German partners specifically structure South African spend to maximise QSAPE qualification.

Nigeria’s NFVCB levies a fee on film productions for certification and censorship approval — a cost rather than a benefit for producers — but Nigeria has not developed a comparable production incentive scheme. The absence is commercially consequential: it limits Nigeria’s attractiveness as a destination for international co-productions that evaluate incentive structures as part of their location economics.

Kenya Film Commission co-production treaty facilitation covers bilateral agreements with Germany, France, and Canada, among others. These treaties allow qualifying Kenyan productions to access foreign co-producer financing and may unlock national film fund eligibility in the partner country — a meaningful capital source for productions structured to meet the relevant criteria.

The structural asymmetry — South Africa with robust incentives, Nigeria and Kenya with limited public financing — shapes the geography of African film finance. Premium co-productions skew toward South Africa; Nollywood’s volume production economy remains built on private investor networks.

BETAR.africa covers Africa’s creative economy with an economic lens. This article is part of an ongoing series on the business models and revenue structures behind Africa’s creative industries.