Nigeria Banks at Day 35: The CBN Blinks, the Courts Are Deciding, and No Buyer Has Moved

By BETAR.africa Business Desk | Publish W/C 4–11 May 2026

Chapter 4 of BETAR’s CBN Recapitalisation Coverage Arc. Chapter 1: Who Made the Cut. Chapter 2: Enforcement Aftermath. Chapter 3: Who Acquires the Failures and at What Price?

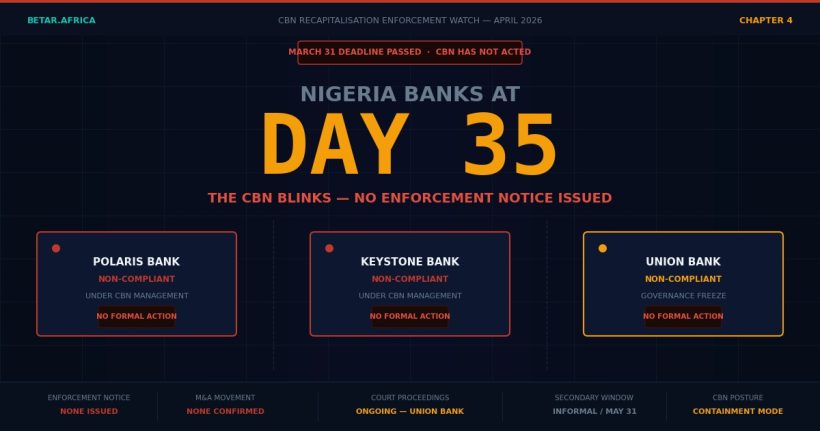

Thirty-five days after Nigeria’s March 31 banking recapitalisation deadline, the Central Bank of Nigeria has not issued a single formal enforcement notice against the three lenders that missed it. No directed merger. No licence revocation. No public announcement of supervisory intervention. What the CBN issued instead, on April 3, was a statement: Polaris Bank, Keystone Bank, and Union Bank “have the capacity to meet the requirements.” The regulator, it appears, is managing down the temperature of a situation it does not yet want to escalate.

That posture has a logic. It also has a clock.

The Regulator’s Containment Mode

In its April 3 statement — carried by ThisDay, AllAfrica, and the ICIR — the CBN did not walk back the enforcement framework it established after the March 31 deadline. It did not grant an extension. What it offered was a form of verbal reassurance: the three non-compliant banks retain what the CBN called “capacity” to achieve compliance, implying that the supervisory process remains active and ongoing rather than terminal.

For market participants and depositors, the practical read is containment. The CBN’s historical pattern in similar situations — the 2005–2006 recapitalisation era, the 2009 banking crisis — has been to use informal bilateral engagement with non-compliant banks before moving to public enforcement action. The April 3 statement suggests that bilateral track is still the primary instrument, even 35 days past deadline.

The risk in that approach is time. The longer the CBN delays formal action, the more it compresses the enforcement clock against the May 31 secondary compliance window that was implied — but never formally announced — in its post-deadline communications. Directed mergers take months to execute. Licence revocations require NDIC coordination. Neither can happen on a four-week runway.

Union Bank: Governance Freeze

The most structurally complicated situation among the three non-compliant banks is Union Bank, where the enforcement question has been overtaken by a governance crisis that the courts are now managing.

The sequence: on March 25, a Federal High Court nullified the CBN-appointed management of Union Bank, ruling that the regulator’s intervention process did not follow statutory requirements and reinstating the pre-intervention board under chairman Alhaji Gumel. The CBN responded within 24 hours, filing an emergency appeal with a six-member Senior Advocate bench — unusual firepower for a mid-tier bank case. By March 28, the CBN had filed a stay motion pending the appeal outcome.

As of early April, the stay has not been ruled on. The operational consequence is ambiguity: neither the CBN-appointed management nor the reinstated Gumel board can execute major decisions — including any recapitalisation transaction — without the other side challenging it. Union Bank is, in effect, governance-frozen until the Court of Appeal rules.

The capital gap is not academic. The CBN’s own affidavit filed in the Union Bank case cited a N224 billion shortfall against the new N500 billion minimum for commercial banks with international authorisation. That figure was current as of the filing date and represents one of the largest individual gaps in the recapitalisation exercise. Resolving Union Bank without a clear governance structure is operationally impossible — which is why the Court of Appeal ruling, not the CBN’s enforcement calendar, is the actual pacing mechanism for this case.

Polaris and Keystone: Silence Where Buyers Should Be

At day 35, there is no public signal of a buyer for either Polaris or Keystone Bank.

None of Nigeria’s Tier-1 lenders — Zenith, GTCO, Access, UBA, First Bank — has issued a statement of interest, filed a required disclosure with the NGX, or mandated an investment bank for a Polaris or Keystone transaction. No acquisition talks have leaked into the market through the normal channels: no banker briefings, no regulatory pre-clearance filings, no preliminary due diligence engagement flagged by advisers.

That silence is consistent with the conclusion BETAR reached in Chapter 3: the most likely resolution path for Polaris and Keystone is not an arm’s-length acquisition by a Tier-1 bank but a CBN-directed merger between the two lenders — a transaction that would require no buyer premium, minimal open-market engagement, and could be executed primarily as a supervisory combination with NDIC backstopping the capital shortfall. Polaris’s capital gap is estimated at approximately N150 billion against its 2022 capital base; Keystone’s figure has not been publicly disclosed by the regulator.

The silence also reflects the market’s read on asset quality. In BETAR’s Chapter 3 analysis, we noted that distressed bank acquisition pricing in Nigeria has historically been anchored to NPL exposure — and Polaris and Keystone carry legacy NPL books that institutional acquirers would require significant haircut protection to absorb. The Heritage Bank NDIC recovery data reinforces that calculus: uninsured Heritage Bank depositors have received N46.6 billion (April 2025) and N24.3 billion (January 2026) in payouts — a cumulative recovery rate of approximately 14.4 kobo per naira. That number is the floor-level reference for what distressed Nigerian bank resolution actually costs.

The Market Is Pricing an Orderly Outcome

Whatever ambiguity surrounds enforcement and governance, the NGX’s banking sector is pricing resolution, not contagion.

The NGX Banking Index crossed 200,000 in early April — a level not seen since before the post-COVID correction — with year-to-date gains concentrated in the sector’s strongest names: Zenith Bank +33.1%, GTCO +24.2%, UBA +12.2%. The market’s interpretation of the enforcement delay is not regulatory weakness; it is evidence that the CBN has sufficient control over the outcome to manage it without a disorderly public default at any of the three non-compliant banks.

That pricing may be correct. It may also be fragile. If the Court of Appeal rules against the CBN’s Union Bank stay and the governance freeze deepens, or if the CBN’s informal bilateral track with Polaris and Keystone fails to produce a transaction structure by June, the market’s orderly-resolution thesis will require revision.

What to Watch Next

Two triggers will determine whether Chapter 5 of this series is an enforcement story or a transaction story.

The first is the Court of Appeal stay ruling on Union Bank. A CBN-favourable outcome restores the regulator’s management control and reopens the recapitalisation transaction process. An adverse ruling deepens the governance freeze and potentially requires legislative intervention or a Supreme Court escalation — either of which moves the resolution timeline into late 2026.

The second is the CBN’s internal enforcement clock on Polaris and Keystone. If the bilateral track does not produce a credible transaction structure by end-May, the regulator will face a choice between announcing a directed merger (visible, disruptive) or extending the informal process further (less disruptive, increasingly credibility-costly). The May-end pressure point is real even if the CBN’s April 3 statement chose not to articulate it.

At day 35, the Nigerian banking recapitalisation story has not concluded. It has merely changed its form: from a compliance deadline story to a courts-and-enforcement story in which the most consequential moves are happening in Federal High Court cause lists and CBN bilateral meeting rooms, not in the public market.

— Business Desk, BETAR.africa

Series navigation: This is Chapter 4 of BETAR’s CBN Recapitalisation Coverage Arc. Related coverage: Chapter 1 — CBN Deadline | Chapter 2 — Enforcement Aftermath | Chapter 3 — Who Acquires the Failures