South Africa’s Fibre Consolidation Is Done. Now the Real Test Begins.

The R11 billion Vodacom-Maziv deal closed in December after four years of regulatory attrition. What Remgro, Vodacom, and South Africa’s 900-plus ISPs do next will determine whether it was worth the wait.

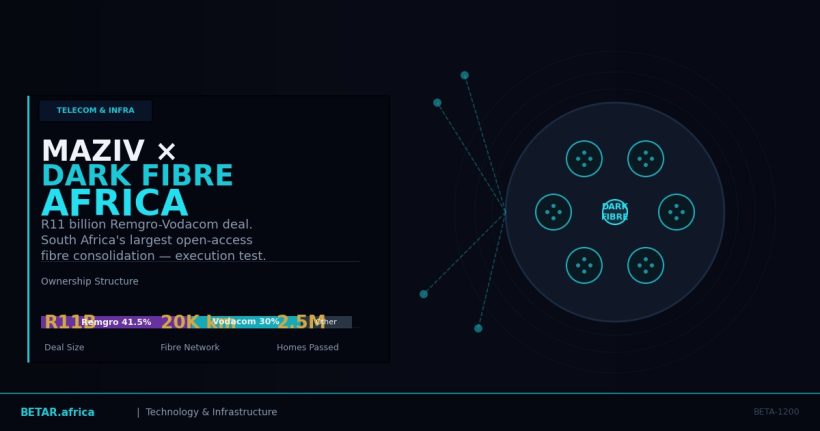

On 1 December 2025, Standard Bank cleared the financial close on one of the largest infrastructure transactions in South African corporate history: Vodacom’s acquisition of a 30% co-controlling stake in Maziv, the combined entity of Vumatel and Dark Fibre Africa, at an R11 billion valuation. ICASA had approved the deal five days earlier, on 26 November, after four years of regulatory contestation — including a Competition Tribunal block in 2024 that nearly killed it entirely.

The deal’s significance extends well beyond the balance sheet. With Vodacom now inside Maziv, South Africa has completed a structural consolidation of its open-access fibre layer that will shape broadband competition, ISP economics, and digital inclusion policy for the better part of a decade.

What Was Built — And What Was Bought

Maziv, formed through the combination of Vumatel and Dark Fibre Africa (DFA) under Remgro’s CIVH holding company, is the largest open-access fibre operator in South Africa. Vumatel currently passes more than 2 million homes, predominantly in urban and peri-urban residential markets. DFA operates over 14,500 kilometres of metro fibre, primarily serving enterprise, government, and mobile tower backhaul — with approximately 12,600 tower sites connected to fibre.

Vodacom’s entry was structured as a combination of existing assets and new cash. The operator contributed R4.89 billion in fibre and transmission assets — effectively bringing its own fibre infrastructure into the Maziv family — and paid R6.11 billion in cash for the balance of the 30% stake. Remgro retained a 57% interest in CIVH post-transaction; Vodacom holds an option to purchase an additional 4.95% stake indirectly, exercisable until March 31, 2027.

For Remgro, the deal delivered an immediate financial dividend. CIVH paid out a R2.66 billion pre-implementation dividend, lifting Remgro’s group cash position to R12.03 billion from R8.36 billion. The deeper payoff was operational: CIVH reported headline earnings of R216 million in the six months to December 2025 — a significant turnaround from a headline loss of R248 million in the comparative period. The fibre infrastructure plays that had consumed capital for years were finally generating positive returns at scale.

The Regulatory Arithmetic

The deal’s tortured regulatory history is instructive. The Competition Tribunal initially blocked it in early 2024 on the grounds that Vodacom’s entry into Maziv would create an entity too dominant to guarantee genuine wholesale market competition. The concern was structural: Vodacom is South Africa’s largest mobile operator and a significant broadband retailer. Having it co-control the country’s largest open-access fibre network created an obvious conflict of interest between the network’s wholesale and retail incentives.

What changed the calculus was a negotiated conditions framework. Rather than a structural block, regulators accepted a set of behavioural obligations that effectively codify what the deal’s proponents now call “Open Access 2.0.”

The conditions require non-discriminatory wholesale access — meaning Vodacom cannot obtain preferential pricing or service terms from Maziv relative to competing ISPs. They mandate pricing oversight mechanisms with cost-based pricing tests. They require mandated coverage expansion into lower-income communities, with time-bound obligations tied to measurable rollout targets. And they impose service quality standards and SLA monitoring commitments enforced by ICASA.

The Competition Commission’s logic was that a large, well-regulated consolidated platform may actually deliver better wholesale market outcomes than a fragmented one — if enforcement is credible. The question South Africa’s 900-plus ISPs are now asking is whether ICASA has the capacity and the appetite to make that enforcement stick.

What the Numbers Say About South African Broadband

Fixed broadband penetration in South Africa sits at roughly 35% of urban households — significant by continental standards, but well below the coverage rates common in peer middle-income economies. The undersupply is most acute in lower-density urban and peri-urban areas where the economics of fibre rollout are marginal without either subsidy or scale.

Vodacom’s entry provides both. The capital infusion — and the signal to debt markets that Maziv’s balance sheet is now partially backstopped by a JSE-listed blue-chip operator — gives Maziv the financial firepower to extend rollout into segments it could not economically service alone. Vumatel has already committed to building the roughly 1 million additional homes passed that it pledged to the Competition Commission as part of the conditions framework.

DFA’s position is equally strengthened. Its 5G backhaul play — the tower fibre connectivity that makes mobile network densification economically viable — is directly aligned with Vodacom’s own 5G rollout agenda. DFA CEO Dietlof Maré has been explicit: “You can’t densify 5G and roll out 5G across South Africa without a fibre solution.” With Vodacom now as a strategic partner rather than an arm’s-length customer, the alignment between DFA’s infrastructure expansion and Vodacom’s network investment cycle is structural, not contractual.

The group’s financial trajectory reflects genuine operational momentum. Consolidated revenue grew 11% to R3.76 billion in the six months to December 2025. EBITDA grew at the same rate, reaching R2.46 billion. Free cash flow before capital expenditure increased 31% to R1.5 billion — the strongest signal yet that the open-access model has reached the scale at which it generates sustainable cash returns.

The ISP Question

The market structure that matters most for South African consumers is not the Vodacom-Maziv bilateral relationship — it is the wholesale ISP ecosystem that depends on Maziv’s infrastructure for last-mile delivery.

Open-access fibre works, when it works, because independent ISPs can compete on service, pricing, and customer experience rather than network ownership. The economics depend on wholesale reference offers that are genuinely cost-reflective and service quality standards that prevent incumbents from self-dealing. In South Africa, that ecosystem has matured considerably: Vumatel alone supports hundreds of ISPs on its network, including substantial competitors to Vodacom’s own retail broadband products.

The risk introduced by the deal is subtle rather than obvious. Vodacom does not need to take overt discriminatory action against competitor ISPs to distort the market. It needs only to be a co-controlling shareholder in the investment decisions about where Maziv builds next — and whether those decisions consistently align with areas where Vodacom’s retail presence is weakest, or where its retail products face the most competitive pressure.

ICASA’s conditions address this risk on paper. The regulator now has formal jurisdiction over Maziv’s wholesale pricing and coverage obligations in a way it did not before the transaction. Whether that jurisdiction translates into meaningful enforcement will be tested over the next 24 months as Maziv begins its accelerated rollout programme and as ISPs file the first complaints under the new framework.

BETAR Analysis: Open Access 2.0

South Africa’s approach to the Vodacom-Maziv deal represents a calculated regulatory bet: that large, consolidated, well-regulated fibre platforms are more likely to deliver universal broadband coverage than a fragmented collection of smaller operators competing for the same high-income urban corridors.

The international precedent is mixed. In Australia, the National Broadband Network’s structural separation model achieved near-universal wholesale access but at a capital cost that was politically unsustainable. In the UK, Openreach’s regulated separation from BT created genuine ISP competition but left rural coverage dependent on subsidy programmes. South Africa is attempting something different — a privately consolidated network with regulated wholesale obligations and no structural separation — and the outcome will be a meaningful data point for other African markets watching how to structure their fibre buildout.

The signs in the short-term financial data are positive. The signs in the long-term competitive structure are conditional. That condition is ICASA’s enforcement credibility, and it is the variable that cannot be read off any balance sheet.

Maziv now passes 2 million homes and carries the financial firepower of Vodacom’s balance sheet. Whether it passes 5 million — and whether the ISPs that serve those homes are genuinely competitive — is a regulatory story, not just an infrastructure one.

Related coverage: Maziv’s R9 Billion Fibre Pledge: Open-Access Infrastructure Execution After the Vodacom Deal