Nigeria Bank M&A Wave 2026: Who Acquires the Recapitalisation Failures and at What Price?

By BETAR.africa Business Desk | 29 March 2026

Chapter 3 of BETAR’s CBN Recapitalisation Coverage Arc. Chapter 1: BETA-1081 — Who Made the Cut. Chapter 2: BETA-1128 — Enforcement Aftermath.

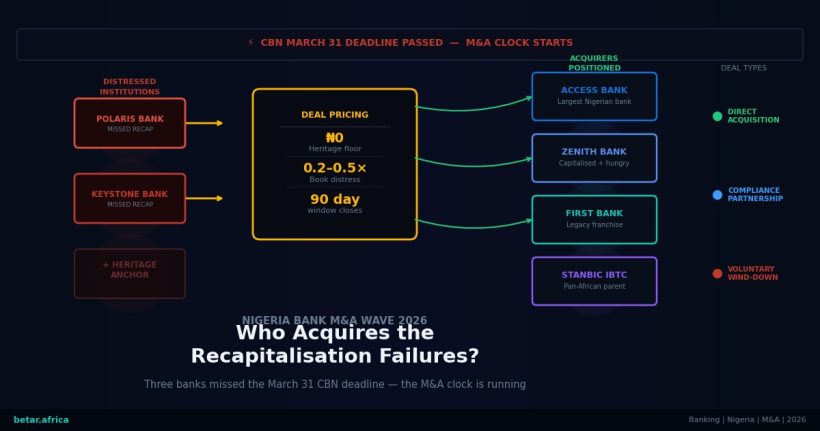

Three Nigerian banks have missed the Central Bank of Nigeria’s March 31 recapitalisation deadline. What happens to them — and who captures their deposits, their branches, their licences, and their liabilities — is the most consequential question in Nigerian banking for the next 90 days. The CBN’s enforcement list is expected in April. When it lands, the M&A clock will start.

To understand the pricing range and the likely acquirers, two questions have to be answered separately. The first is what distressed Nigerian bank assets are actually worth. The second is which institutions are positioned — financially, strategically, and culturally — to absorb them.

The Pricing Floor: Heritage Bank Sets the Anchor

The correct starting point for any Nigerian distressed-bank valuation analysis in 2026 is not a DCF model. It is Heritage Bank.

In May 2024, the CBN revoked Heritage Bank’s operating licence after the institution failed to meet its capital requirements and, critically, could not identify a merger partner or recapitalise independently. The resolution outcome was textbook liquidation: zero enterprise value, Nigeria Deposit Insurance Corporation (NDIC) payout to depositors, employee separation, and branch closure. Heritage Bank’s shareholders received nothing.

That zero-enterprise-value outcome is the pricing floor for Polaris Bank and Keystone Bank as they enter the enforcement window. It is not the expected outcome — the CBN has explicitly signalled it prefers a directed consolidation to a Heritage Bank repeat, which costs the government’s deposit insurance mechanism and creates depositor disruption — but it is the baseline from which any negotiation with a willing buyer begins. An acquirer who knows that the alternative to their offer is NDIC liquidation holds the dominant bargaining position. The sellers — or rather, the CBN-supervised management structures overseeing these institutions — know it too.

The Buyers: A Differentiated Analysis

Not every Tier-1 Nigerian bank is equally positioned to absorb a distressed mid-tier acquisition. The candidate list narrows quickly when acquisition track record, capital position, and strategic logic are applied simultaneously.

Access Bank: The only credible institutional precedent. In 2019, Access Bank acquired Diamond Bank — a transaction that took the merged institution to the top of Nigeria’s asset league table and is, to date, the most complex bank-to-bank integration successfully executed in the country’s post-Soludo history. Access Bank has N500 billion-plus in capital headroom following its 2025 recapitalisation raise, a centralised integration playbook, and management that has lived through the Diamond Bank experience and retains the institutional memory. Of all Nigeria’s Tier-1 banks, Access Bank is the only one for which acquiring a non-compliant mid-tier institution is not a novel operational challenge. Its West African expansion posture — 42-plus transactions across its institutional history — confirms an appetite for deal complexity that its peers have not demonstrated.

Zenith Bank: Capital but wrong model. Zenith Bank’s recapitalisation position is strong and its asset quality is Nigeria’s highest among major commercial banks. But Zenith has built its franchise on an organic growth model — conservative credit culture, top-of-market fee income, premium corporate relationships. The Zenith playbook requires clean counterparties, not distressed ones. Absorbing Polaris or Keystone would introduce non-performing loan ratios, branch networks built for retail traffic that Zenith does not serve at scale, and integration risk that is structurally misaligned with the institution’s operating model. Zenith is not an obvious buyer.

GTCO: Brand tension with mass-market integration. Guaranty Trust Holding Company’s banking subsidiary has spent a decade building brand equity in premium retail and SME segments. The Polaris and Keystone customer bases — community banking, small-value deposits, informal-sector SMEs — are not the GTCO customer profile. An acquisition would dilute the brand positioning that GTCO has carefully constructed and force integration of a mass-market banking operation that sits outside GTCO’s core competence. Unless the CBN structures a transaction with significant concessions, GTCO’s strategic logic does not point toward a distressed acquisition.

Fidelity Bank: The dark horse. Fidelity Bank is not at the top of most acquisition speculation lists, but the structural logic is compelling. Fidelity has national branch coverage, a demonstrated appetite for SME and retail banking segments that overlap with the Polaris/Keystone footprint, and a capital raise that — while smaller than Access Bank’s — has left it with room for a selective acquisition. A Polaris or Keystone branch network in its core operating territories would not require Fidelity to pivot its business model. The integration complexity would be lower than at Access Bank’s scale, but the strategic fit is genuine.

Polaris and Keystone: The Directed Merger Scenario

The CBN’s most likely resolution path for Polaris Bank and Keystone Bank is not an immediate sale to a Tier-1 acquirer. It is a directed merger between the two institutions, under CBN supervision and AMCON support, creating a combined mid-tier bank that is then placed for eventual acquisition on a longer timeline.

Both institutions share indirect structural linkages through the Sigma Golf Group, the investment vehicle connected to their respective AMCON arrangements. A Polaris-Keystone merger would create a combined entity with an estimated N700 billion to N1 trillion in deposits — large enough to function as a viable national-licence bank and to present an acquirer with a consolidated asset rather than two separate distressed transactions. The CBN’s precedent for this model is the 2021 Unity-Providus merger, where a N700 billion bridge facility supported consolidation of two under-capitalised institutions into a single entity that subsequently stabilised.

An AMCON-supported Polaris-Keystone entity, stabilised over 12 to 18 months, then becomes a credible acquisition target for Access Bank or Fidelity in a structured transaction with regulatory concessional support — potentially including NPL backstops, tax reliefs, or preferential licence terms.

Union Bank: Litigation as Leverage

Union Bank of Nigeria’s situation is distinct from Polaris and Keystone in one critical respect: it has shareholders with capital and a strategic interest in the outcome.

The Federal High Court injunction reinstating Union Bank’s board — issued on March 25 — should be read primarily as a negotiating instrument, not as a genuine legal challenge to CBN authority. The principal shareholders — Titan Trust Bank, Luxis International, and Magna International — acquired their stakes at a price that reflects an expectation of value realisation. An NDIC liquidation at Heritage Bank terms would destroy that value entirely. Their interest is to force a resolution that preserves as much equity value as possible, even within a CBN-mandated restructuring.

That is what the court injunction accomplishes: it gives the shareholder group a procedural argument that slows the CBN’s timeline and creates a negotiating space. CBN Governor Olayemi Cardoso has publicly and repeatedly emphasised that the recapitalisation framework is a systemic requirement, not a political one. The appellate process will likely resolve in the CBN’s favour. But the timeline for that resolution — months, not weeks — creates room for a negotiated outcome: Titan Trust Group brings additional capital, the CBN agrees to a modified compliance path, and Union Bank avoids liquidation through a shareholder-led recapitalisation rather than a directed sale.

Concentration Arithmetic and Regulatory Tension

Any resolution of the three non-compliant institutions that routes them into the existing Tier-1 banking structure will accelerate an already significant concentration dynamic in Nigerian banking. Nigeria’s five largest banks — Access Bank, Zenith, GTCO, First Bank, and UBA — currently account for an estimated 85% of the sector’s annual pre-tax profit and 99.96% of total banking assets by CBN classification.

The CBN is aware of this tension: the recapitalisation framework was designed to strengthen the system, not to homogenise it. Requiring banks to hold higher capital inherently advantages incumbents with deeper balance sheets, and a wave of mid-tier acquisitions by top-five institutions moves Nigeria further from the distributed banking sector that serves SMEs, agriculture, and informal-economy participants in ways that concentration does not.

Whether the regulator will impose structural conditions on approval — branch disposal requirements, geographic caps, SME lending ratios — as the price of allowing top-tier banks to absorb mid-tier failures is the open structural question. The CBN has the tools. Whether it uses them will shape Nigeria’s banking landscape for the decade ahead.

BETAR Assessment

Our base-case scenario: the CBN directs a Polaris-Keystone merger by Q3 2026, supported by an AMCON bridge facility structured similarly to the Unity-Providus template. The merged entity is stabilised over 12 to 18 months and placed for acquisition by Access Bank or Fidelity Bank in 2027–2028, with concessional CBN support as an acquisition incentive.

For Union Bank, our read is a negotiated recapitalisation: the Titan Trust shareholder group brings fresh capital under a CBN-approved timeline extension, the court process provides cover for a better-structured resolution, and Union Bank avoids liquidation as a functioning franchise — significantly smaller, governance-restructured, but surviving.

The trigger event that accelerates all three timelines: a formal CBN directive on Polaris and Keystone in April. When that announcement lands, publication of BETAR’s Chapter 3 analysis will be immediate.

BETAR Africa | Business Desk analysis. Related: BETA-1081 — Pre-Deadline (Published 28 March) · BETA-1128 — Enforcement Aftermath · BETA-1069 — Africa Bank-Fintech M&A 2026 · BETA-1041 — MTN IHS Towers Buyout.