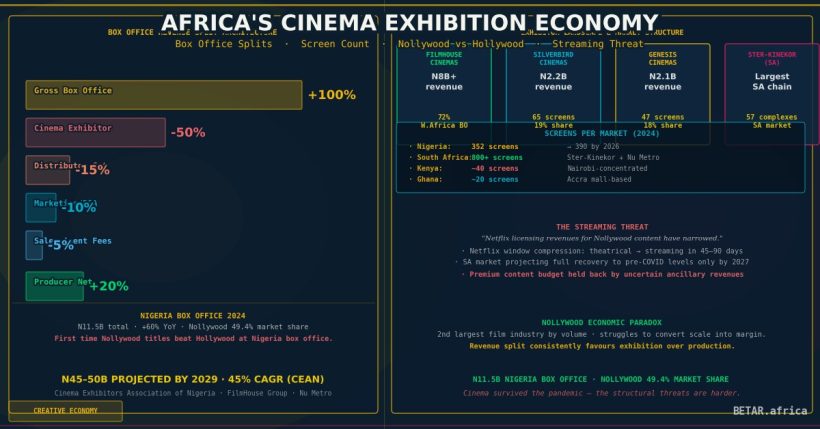

Nigeria’s cinema sector generated N11.5 billion in box office revenue in 2024 — a 60% increase on the prior year and the clearest evidence yet that West Africa’s theatrical market has not only survived the pandemic but rebuilt itself into something commercially significant. For the first time, Nollywood-produced titles captured more of that box office than Hollywood, taking a 49.4% market share against Hollywood’s 48.8%.

The numbers look like a success story. They are, partly. But beneath the headline growth sits a set of structural realities that complicate the narrative: a screen count too thin to support scale, a revenue split that consistently favours exhibition over production, a Netflix licensing market that has narrowed, and a South African industry still projecting recovery to pre-COVID levels only by 2027.

“We have recorded 60 per cent growth in revenue in 2024 and about 4.5 per cent growth in admissions despite the harsh economic climate,” said Ope Ajayi, National Chairman of the Cinema Exhibitors Association of Nigeria (CEAN). Ajayi projects the market will reach N45 to N50 billion in annual box office revenue within four years, at a compounding growth rate of 45%.

The Exhibitor Landscape

Nigeria dominates West African theatrical exhibition. The country accounts for approximately 92% of cinema screens in Anglophone West Africa, with approximately 352 screens across 2024 — projected to reach 390 by 2026.

Three chains define the market. FilmHouse Cinemas, the country’s largest operator, held approximately 72% of West Africa’s total box office in 2025, generating over N8 billion in revenue from 1.4 million admissions. Its top-grossing locations — FilmHouse Lekki (N1.08 billion) and FilmHouse Surulere (N662 million) — demonstrate the revenue concentration within Lagos. The Filmhouse Group, which includes film distribution arm FilmOne Entertainment, is targeting $50 million in group revenue by 2030. “Our cinema business forms the backbone of a broader ecosystem,” Kene Okwuosa, Group CEO of Filmhouse, told industry stakeholders at Cannes 2024.

Silverbird Cinemas operates 65 screens across 10 locations in Nigeria, Ghana, and Liberia, generating approximately N2.2 billion in Nigerian box office in 2024 — a 19% market share. Genesis Cinemas, with 47 screens across 9-12 locations, generated a comparable N2.1 to N2.2 billion, claiming roughly 18% of the market.

South Africa’s exhibition landscape differs structurally. Ster-Kinekor dominates with 57 commercial cinema complexes — by far the continent’s largest single-country operator. Nu Metro, the second-largest, operates 22-plus complexes with 152-plus screens across South Africa, Zambia, and Mozambique, and is actively expanding. The South African market was the first on the continent to develop multiplex cinema at scale, and it remains the most technically sophisticated — Nu Metro installed the first ScreenX auditorium in South Africa in 2025 through a CJ 4DPLEX partnership.

The Revenue Split

Understanding who earns what from a cinema ticket requires tracing a standard distribution waterfall.

In Nigeria, the cinema chain takes 50% of gross ticket revenue in week one of a film’s run, with that share rising to 55% in week two and continuing upward toward 70% in weeks three and beyond. The remaining revenue flows to the distributor-producer side: the distributor typically extracts 15-20% of what the producer receives after the exhibitor cut, with the producer keeping the balance.

In practice: a Nollywood film that generates N1 billion at the box office delivers approximately N500-600 million to the cinema chain in week one economics. Of the remaining N400-500 million, the distributor takes N60-100 million, leaving the producer with roughly N300-400 million before recouping production costs. For a mid-range Nollywood production budgeted at N100-200 million, that return is commercially meaningful — if the film performs.

Hollywood studio titles distributed through Nigeria — Warner Bros. and Disney are both handled locally by FilmOne Entertainment — operate under separate terms that FilmOne negotiates directly with the studios. In 2023, Warner Bros. and Disney combined accounted for 66% of the Nigerian cinema market by revenue; FilmOne managed both slates. The studios’ leverage over local distributors typically results in more favourable revenue terms for the studios than Nollywood independents secure, though the specific percentages are not publicly disclosed.

The Nollywood Box Office Ceiling

The performance ceiling for Nollywood theatrical releases is defined by a small number of films. Funke Akindele’s Behind the Scenes set the all-time Nollywood box office record in 2025 at N2.72 billion. Her prior film, Everybody Loves Jenifa (2024, N1.88 billion), was the only Nollywood title to cross N1 billion in 2024. A Tribe Called Judah, which first crossed the N1 billion threshold in early 2024 with combined Nigerian and UK returns of approximately N1.5 billion, marked the earlier milestone.

At 2024 exchange rates, N1 billion equates to approximately $620,000-$650,000. The frequently cited “$3-5 million” figure for top Nollywood box office performers reflects older exchange rates or combined diaspora theatrical and digital revenues — not contemporary Nigerian box office alone. The naira’s depreciation has materially compressed the dollar value of Nollywood’s commercial success.

The implication for producer economics is significant. A Nollywood producer who generated N300-400 million in theatrical returns in 2024 captured roughly $190,000-$250,000 — before production cost recoupment and before considering what the same film might have earned on a streaming licensing deal.

Streaming vs. Theatrical: The Producer’s Calculation

Netflix’s standard licensing fee for Nollywood films sits in the $10,000 to $90,000 range for acquisition deals — with high-profile original commissions historically reaching higher. But filmmaker Kunle Afolayan stated publicly in 2024 that Netflix has cut back its direct funding of Nigerian productions, shifting toward rights acquisitions of already-completed films at lower price points.

The economics comparison is clarifying. A mid-tier Nollywood production generating N250-500 million at the box office — a reasonable outcome for a well-reviewed commercial film that is not a marquee event — yields its producer perhaps N75-150 million after exhibitor and distributor cuts, or approximately $47,000-$95,000. A Netflix licensing deal for the same film might offer $50,000-$70,000 upfront, without box office risk, without the marketing spend required to drive theatrical admissions, and without the naira exchange exposure.

For all but the top tier of Nollywood producers, the streaming route frequently outperforms theatrical on a risk-adjusted basis. The market response has been a hybrid model: theatrical window first (typically four to eight weeks), then streaming license, then YouTube long-tail revenue from ad-supported playback. Theatrical is no longer the primary revenue event for most Nollywood productions — it is the first event in a multi-platform revenue sequence.

The South African Contrast

South Africa’s theatrical sector presents a starkly different trajectory. The country’s cinema market — mature, multiplex-anchored, and deeply integrated with Hollywood’s global release calendar — was structurally dependent on Hollywood output that the 2023 writers’ and actors’ strikes compressed significantly.

“We’re sitting at 63% of pre-COVID box office levels here,” Ster-Kinekor CEO Mark Sardi noted in mid-2024, while the United States was recovering to 69%. Sardi oversaw a Section 189 restructuring that year — 52 employees retrenched, two cinemas closed — as the company managed through sub-scale attendance. PwC’s Africa Entertainment and Media Outlook projects South African cinema to return to pre-COVID revenue levels only by 2027.

The loadshedding context compounds the issue: South Africa’s rolling power cuts suppressed discretionary leisure activity throughout 2023-2024. Nu Metro’s expansion strategy — opening premium-format locations and re-entering sites vacated by Ster-Kinekor — represents a bet that consolidated supply in the right locations can sustain margins even on reduced aggregate admissions.

The Screen Count Constraint

Africa’s fundamental cinema economics challenge is visible in a single comparison: the continent has approximately 1,500 to 1,700 screens for 1.4 billion people, versus approximately 40,000 screens for the 330 million people in the United States. The US has roughly 110 screens per million residents; Africa has roughly one.

The constraint is not cultural appetite. Nigeria’s 2024 admissions of 2.66 million — an increase on the prior year — were generated from fewer than 400 screens in a country of 220 million people. The latent demand that a broader screen footprint would unlock is substantial. But cinema construction economics are hard: multiplexes require anchor retail environments (or purpose-built real estate), reliable electricity supply, and local currency financing in markets where commercial lending rates frequently exceed 20%.

CEAN’s Ajayi projects a N45-50 billion Nigerian box office within four years. Achieving that target requires both the continued cultural ascendance of Nollywood content and a meaningful expansion of screen capacity beyond current trajectories. Without more screens, the box office ceiling is set by venue physics as much as audience appetite.

Named sources: Ope Ajayi, National Chairman, Cinema Exhibitors Association of Nigeria (CEAN); Kene Okwuosa, Group CEO, Filmhouse Group; Mark Sardi, CEO, Ster-Kinekor.