Before a single regulator issued a formal directive, Nigerian banks and mobile network operators had already refunded more than ₦10 billion to customers for failed airtime and data transactions. That figure — revealed when the Nigerian Communications Commission (NCC) and the Central Bank of Nigeria (CBN) jointly unveiled their new refund framework in January 2026 — is both a rebuke and a road map.

The refunds happened because two regulators went looking. Now they have built a system designed to make looking unnecessary.

What the Framework Requires

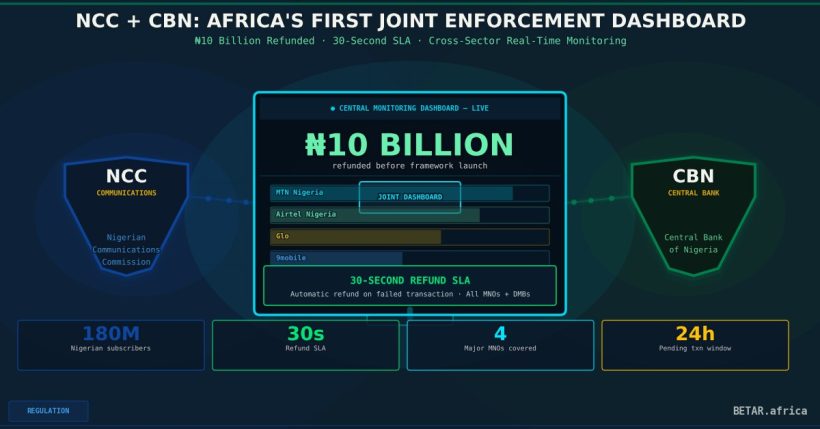

The NCC-CBN Consumer Refund Framework, announced January 9 and effective from March 1, 2026, mandates that any subscriber debited for airtime or data who does not receive value is entitled to an automatic refund within 30 seconds — the time it takes to recognise a failed transaction at the network level.

There is one exception: transactions classified as “pending” — typically those caught between a bank’s payment switch and an operator’s provisioning system — may take up to 24 hours to resolve. All other failures are subject to the 30-second SLA.

The framework applies to:

- All four major MNOs — MTN Nigeria, Airtel Nigeria, Glo, and 9mobile

- Value Added Service (VAS) providers licensed under the NCC

- All Deposit Money Banks (DMBs) under CBN supervision

Operators are also required to send customers an SMS notification for every transaction — success or failure — within the same 30-second window. The notification requirement closes a gap that has historically let failed transactions go undetected by subscribers: many Nigerians discover a missing top-up hours later, if at all.

The Compliance Architecture: A Joint Dashboard

The most significant regulatory innovation in the framework is not the refund timeline — it is the enforcement infrastructure that sits behind it.

The NCC and CBN are jointly operating a Central Monitoring Dashboard that logs transaction failures, tracks refund timelines, and identifies responsible parties in real time. The dashboard receives data from both MNOs and DMBs, enabling the two regulators to cross-reference a failure event: if a subscriber is debited at the bank level but the operator’s system shows no provisioning request, the fault is clearly on the banking side. If a bank shows a successful transfer to an operator’s billing system but no airtime was credited, the fault sits with the operator.

This bilateral attribution is the architectural breakthrough. Nigeria’s previous regime for addressing failed telecom transactions lacked a shared data layer between the two regulatory domains. Consumers who were debited by their bank but received nothing from their operator faced a circular blame structure: operators pointed at banks, banks pointed at operators, and the complaint fell into an administrative gap that neither regulator had direct visibility into.

The Joint Dashboard eliminates that gap. For the first time in Nigeria — and to BETAR’s knowledge, across Africa — a single monitoring system tracks the handoff between financial services and telecommunications infrastructure at the individual transaction level.

₦10 Billion: The Scale of a Hidden Problem

The ₦10 billion refund figure disclosed at the January launch is striking because it preceded the framework’s March 1 deadline. The money was disbursed in anticipation of — or under informal pressure from — the regulators’ investigation into historical transaction failures. The disclosure was made by the NCC as part of its case for formalising the framework: this was not a hypothetical consumer protection problem. It was an active one, operating at scale, without visibility.

To put the figure in context: Nigeria has approximately 180 million telecom subscribers and the country processes billions of airtime and data transactions annually. The ₦10 billion refunded likely represents only the failures that were identified and attributed through the regulators’ pre-announcement audit. How much remains unrefunded — or was simply absorbed as customer loss — is unknown.

The framework’s 30-second SLA and mandatory SMS notification are designed to ensure that every future failure becomes visible, immediately, to both the subscriber and the regulator. Failures that previously disappeared into system logs will now generate real-time data on the Joint Dashboard.

Who Gets Penalised When It Fails?

The framework’s SLA structure creates explicit accountability. Operators and banks are bound by enforceable agreements that define fault attribution based on where in the transaction chain the failure occurred. The NCC retains enforcement authority over MNOs and VAS providers; the CBN retains authority over DMBs.

The penalty regime follows each regulator’s existing enforcement framework:

- NCC penalties for licensed operators who miss SLAs draw on the Nigerian Communications Act and the NCC’s Consumer Code of Practice Regulations, which allow administrative fines scaled to breach severity.

- CBN penalties for banks draw on the Banks and Other Financial Institutions Act (BOFIA) 2020 and the CBN’s Consumer Protection Framework.

What the joint framework introduces is the shared attribution layer — the dashboard that tells each regulator whose failure to penalise. This closes the escape hatch. An operator that previously argued “the bank’s system delayed the provisioning request” can now be tested against the dashboard record.

Why This Architecture Matters Beyond Nigeria

Nigeria is not the only African market where mobile airtime and data transactions cross the bank-telecoms regulatory boundary. The same architecture — subscribers paying through bank accounts or mobile money wallets, operators provisioning on a separate network — exists in Kenya, Ghana, South Africa, and across much of Francophone West Africa.

What distinguishes this framework is the formalised joint oversight model. Regulators in most African markets operate in silos: telecoms authorities do not typically share real-time data with central banks, and vice versa. The NCC-CBN arrangement is a template that other regulators could adopt for any transaction category that crosses the two domains — mobile money recharges, bill payments, and ultimately, digital financial services more broadly.

The ECOWAS Supplementary Act on Consumer Protection in Electronic Commerce has long called for cross-sector consumer redress mechanisms. Nigeria’s joint dashboard is, functionally, what that looks like when it is built.

The Compliance Reality for Operators

For MNOs and banks, the March 1 go-live represented a significant technical integration effort. Operators must feed transaction-level data to the NCC’s node on the Joint Dashboard; banks must feed transaction-level data to the CBN’s node. The two data streams are reconciled in real time.

Any operator or DMB not fully integrated with the dashboard as of March 1 faces a compliance exposure: SLA breaches will go unpunished, but the dashboard will also have no record of their transactions, creating a separate audit liability.

The framework is also not static. The NCC and CBN have signalled that the monitoring dashboard will evolve — its initial scope covers airtime and data transactions, but the architecture is designed to accommodate additional transaction categories.

For Nigeria’s fintech sector, this last point is material. Any product that routes through an MNO billing system or a bank’s payment switch — mobile-first bill payment apps, USSD-based services, and bank-to-telco money flows — sits within scope of the framework’s underlying compliance logic, even if not yet explicitly covered.

The Bottom Line

The NCC/CBN Joint Refund Framework is not primarily a consumer protection measure, though it functions as one. It is, more precisely, an enforcement architecture built to resolve a regulatory blindspot that had persisted for years: the gap between the domain of telecoms oversight and the domain of banking oversight, through which ₦10 billion in consumer harm had already passed before anyone built the dashboard to see it.

Twelve days after go-live, the framework is operational. Whether it is working — whether the 30-second SLA is being met, whether the Joint Dashboard is correctly attributing failures — will be tested in the coming months. The regulators have the infrastructure to find out.

BETAR.africa tracks regulatory developments across all 54 African nations. Sources: NCC/CBN joint circular (January 2026); Technext, Nairametrics, TechCabal, Techpoint, Premium Times Nigeria (January–March 2026).