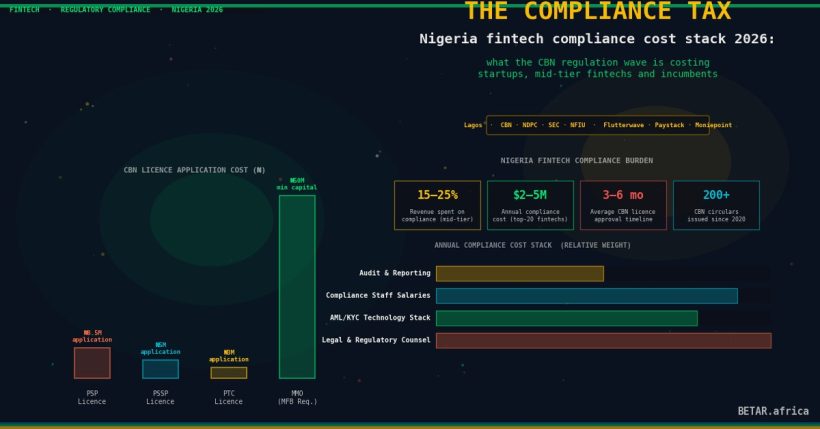

Between January and March 2026, the Central Bank of Nigeria issued four major compliance mandates in rapid succession. Each, taken individually, was defensible as prudent regulatory modernisation. Together, they constitute the heaviest compliance cost stack ever imposed on Nigerian fintech in a single quarter — and for smaller operators without the engineering bench or compliance infrastructure to absorb them, the window to survive is closing faster than the deadlines suggest.

BETAR has mapped each regulatory layer, its implementation timeline, and its cost implications, drawing on Nigeria’s published compliance cost modelling for a baseline 100,000 active-user fintech operation. The picture that emerges is not simply one of higher operating costs. It is a story about which business models can absorb the shock, which will pass it on to customers, and which are structurally incompatible with the new regulatory environment.

Four Mandates, One Quarter

The sequence began with the Virtual Assets Regulatory Amendment (VARA) framework, which came into force in January 2026 and imposed full compliance obligations — including enhanced AML controls and mandatory transaction monitoring — on all virtual asset service providers licensed or operating in Nigeria. Unlike previous CBN guidance on crypto, VARA has enforcement teeth: non-compliant platforms face licence suspension rather than advisory sanctions.

In February, the CBN issued a deadline for the BVN phone number lock: from May 1, 2026, every account opening and material transaction must match the customer’s BVN-linked phone number in real time. The goal is to close a known fraud vector where SIM-swap attacks allow bad actors to intercept OTP codes on accounts where phone numbers have drifted from BVN records. Implementation requires integration with the Nigeria Inter-Bank Settlement System (NIBSS) verification API — infrastructure that exists and works, but whose per-call cost is not trivial at scale.

March brought two further mandates. The AI and Anti-Money Laundering Baseline Standards require all payment service banks and licensed fintech operators to deploy machine-learning-based transaction monitoring by a phased June 2026 deadline — including model documentation, annual validation by an independent third party, and a data governance framework. One week later, CBN circular BSD/DIR/PUB/LAB/004/026 mandated liveness checks (biometric verification that the applicant is a live human, not a photograph or deepfake) for all digital account openings, effective July 1, 2026.

Four mandates. Three months. Five distinct implementation deadlines between May and July.

The Cost Stack, Layer by Layer

BETAR’s compliance cost model uses a baseline of 100,000 active users and 10,000 new account openings per month — parameters consistent with a mid-tier Nigerian neobank or wallet operator.

Layer 1 — VARA (active): For operators in scope, VARA compliance requires a licensed VASP officer, enhanced KYC for all virtual asset transactions, and real-time reporting infrastructure. Estimated ongoing cost: ₦12–25 million annually in Nigeria, depending on transaction volume and whether an in-house compliance officer or a licensed third-party administrator is used.

Layer 2 — BVN phone lock (May 1 deadline): Setup cost for NIBSS API integration runs ₦8–25 million one-time across engineering and certification. Per-verification call cost: ₦85–260 (approximately $0.05–$0.15 at current rates). At 10,000 new account openings per month, plus ongoing transaction verification triggers, annual steady-state cost for a mid-size operator is estimated at ₦20–60 million.

Layer 3 — AI/AML baseline standards (June deadline): This is the heaviest single cost layer. A compliant transaction monitoring platform — Sardine, ComplyAdvantage, Themis, or a locally-built equivalent — costs $12,000–$30,000 annually at mid-tier scale. Annual independent model validation, as explicitly required by the CBN circular, adds $15,000–$40,000. Legal and documentation overhead to produce the required model risk management framework: $8,000–$20,000 in year one, declining thereafter. Total year-one cost for AI/AML compliance: $35,000–$90,000.

Layer 4 — Liveness checks (July 1 deadline): Biometric liveness verification APIs (Smile Identity, Trulioo, Aware) charge $0.10–$0.50 per verification. At 10,000 new account openings monthly, that is $12,000–$60,000 per year at current pricing. Volume discounts reduce this meaningfully for larger operators; they do not help smaller ones.

Aggregated across all four layers, BETAR estimates year-one compliance costs for a bootstrapped mid-tier Nigerian fintech at $52,000–$87,000 in build costs plus $24,000–$48,000 in annual steady-state costs at current scale. For operators engaging external fintech counsel — considered prudent given the criminal liability provisions in the VARA and AI/AML frameworks — year-one total rises to $120,000–$200,000.

Who Pays, and Who Absorbs

Not every cost lands in the same part of the P&L, and the distinction matters for how operators respond.

Liveness check costs are per-acquisition: they hit the customer acquisition cost (CAC) line directly. An operator paying $0.30 per liveness check on a product where customer lifetime value is $4 will feel the squeeze immediately. The obvious response — raising account fees or tightening acquisition criteria — reduces financial inclusion reach, which is precisely the outcome regulators say they want to avoid.

The BVN phone-lock cost is partly fixed (integration), partly variable (per-verification call). It is broadly absorbable for large operators who spread it across a substantial user base; for operators below roughly 50,000 active users, the per-user economics are punishing.

The AI/AML model validation cost is the most regressive element of the entire stack. Independent validation runs at roughly the same price whether the operator has 20,000 or 2 million users. It is a fixed cost that inherently penalises smaller players — a structural dynamic that regulators appear to have accepted as the price of systemic safety.

VARA compliance costs are absorbed almost entirely as overhead for in-scope operators. There is no clear pass-through mechanism; the market is not pricing VASP compliance as a fee-bearing service.

Which Business Models Break

The four mandates do not affect all fintech models equally. Three categories face acute exposure.

Digital lenders are the most exposed category overall, for a counterintuitive reason: they are newly brought into the full AI/AML framework in a way that wallet operators were not previously. Lending platforms that built their ML infrastructure for credit scoring — not transaction monitoring — must now retrofit or replace systems to meet CBN model governance standards by June. The engineering burden is non-trivial, and the models are substantively different.

USSD-based microfinance banks face a product design crisis. Liveness checks are biometric — they require a camera, or at minimum a device capable of running a biometric SDK. USSD, by definition, is text-only. MFBs whose core onboarding flow runs on USSD must either rebuild their customer journey around a smartphone-first experience or seek an exemption that the CBN has not yet signalled it will grant.

Crypto exchanges are the outlier case: they face the full weight of all four mandates simultaneously. VARA applies to them by definition. BVN phone-lock and liveness checks apply to onboarding. AI/AML standards apply to transaction monitoring. The handful of Nigerian exchanges with active CBN or SEC licences — Yellow Card, Quidax, Busha — have the infrastructure to absorb this. Unlicensed operators or platforms operating in grey zones effectively cannot comply and face exit.

Is Consolidation the Consequence?

Compliance as consolidation force is a thesis that African fintech analysts have floated for two years. The Nigerian Q1 2026 regulatory wave may be the empirical test case. The argument runs as follows: compliance costs create a scale threshold below which operation becomes economically irrational. Operators below that threshold either raise capital (unlikely in the current equity environment, per BETA-566), find an acquirer, or wind down.

The counter-argument is that African fintech has a long history of absorbing compliance costs through operational creativity — shared compliance infrastructure, cooperative KYC utilities, and informal arrangements that regulators tolerate. Nigeria’s NIBSS infrastructure is precisely one such shared utility. If the CBN were to extend the BVN verification API subsidy or create a compliance sandbox for smaller operators, the consolidation thesis weakens significantly.

What is not in dispute is the direction of travel. The era of operating a Nigerian fintech on minimal compliance infrastructure — the era that allowed neobanks to undercut incumbent bank fees by routing around their compliance costs — is over. The regulators have explicitly decided to impose bank-equivalent standards on bank-equivalent activities. Whether that produces a safer, more sustainable sector or a less competitive, less inclusive one depends on how implementation is managed in the months ahead.

BETAR’s Nigeria Fintech Compliance Cost Stack model draws on the published CBN circulars BSD/DIR/PUB/LAB/001–004/026, the VARA framework (January 2026), and vendor pricing data from Smile Identity, ComplyAdvantage, Sardine, and NIBSS public tariff documentation. Currency conversions at March 2026 rates (₦1,700/$1 indicative). See also: BETA-624, BETA-623, BETA-694, BETA-611.