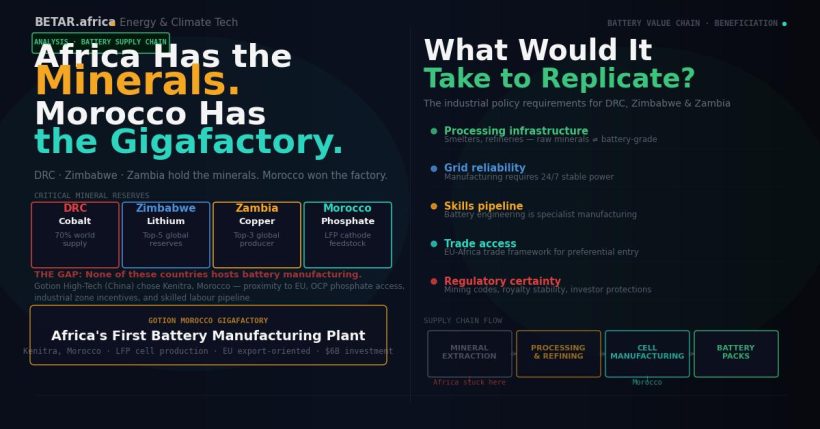

Africa Has the Battery Minerals. Morocco Has the Gigafactory. Here Is the Gap.

The Democratic Republic of Congo holds 70 per cent of the world’s cobalt. Zimbabwe is sitting on one of the largest lithium deposits outside South America. Zambia is among the world’s top copper producers. None of them has Africa’s first battery gigafactory. Morocco does. The question is not why — it is what fixing that gap would actually require.

When Gotion High-Tech begins battery cell production in Kenitra, Morocco in the third quarter of 2026, it will mark the first time a lithium battery cell has been manufactured on African soil. The factory — a $5.6 billion complex capable of 100 gigawatt-hours of annual output at full build-out — has been extensively covered as a Morocco story. It is not, primarily, a Morocco story.

It is a story about a continent that supplies the raw materials for a global technology revolution and captures almost none of the manufacturing value. And it raises a question that Morocco’s gigafactory makes impossible to avoid: if the Democratic Republic of Congo, Zimbabwe, and Zambia together hold the world’s most concentrated deposits of cobalt, lithium, and copper — the essential inputs for the batteries that will power the next fifty years of energy and transport — why is Africa’s first battery gigafactory in a country that has none of those minerals?

Morocco’s Minerals Argument (It Is Not Nothing)

Morocco’s claim to battery industry relevance is narrower but more substantive than it first appears. The Gotion facility produces lithium iron phosphate cells — LFP chemistry, which does not use cobalt. LFP batteries require three primary inputs: lithium, iron, and phosphate. Morocco has no lithium deposits of significance. It has abundant iron. And it holds approximately 70 per cent of the world’s known phosphate rock reserves, according to the United States Geological Survey’s 2025 Mineral Commodity Summaries — the largest strategic mineral stockpile in any single country for any battery-relevant material.

Phosphoric acid is a critical intermediate in LFP cathode production. Morocco’s Office Chérifien des Phosphates (OCP Group), the world’s largest phosphate exporter, has been positioning itself explicitly as a battery supply chain player since 2023, announcing partnerships with Chinese battery material firms and piloting cathode precursor production at its Jorf Lasfar industrial complex. Gotion’s choice of LFP chemistry is not incidental to its choice of Morocco. The phosphate supply chain is local in a way that lithium, cobalt, and manganese are not.

This matters for the honest assessment of the Kenitra investment. Morocco is not merely a location of convenience — it has a genuine upstream feedstock advantage for the specific battery chemistry Gotion has deployed. But that advantage does not extend to lithium. And lithium is the mineral that defines who controls the battery supply chain.

Where Gotion’s Lithium Actually Comes From

Battery-grade lithium carbonate and lithium hydroxide — the processed forms that feed into cathode production — come overwhelmingly from Australia, Chile, and Argentina at the mine stage, with processing concentrated in China. Gotion High-Tech, as a Chinese manufacturer with its primary supply chain relationships anchored in Hefei and the Yangtze River Delta industrial belt, sources its lithium through Chinese processing intermediaries regardless of where the spodumene or brine originates.

Zimbabwe is theoretically in that supply chain. Chinese firms — Sinomine Resource Group at Bikita Minerals, Huayou International at Arcadia, and Zhejiang Huayou Cobalt at Sabi Star — have acquired the majority of Zimbabwe’s most productive lithium deposits since 2021. Zimbabwe produced approximately 800,000 tonnes of lithium ore in 2024, according to the Zimbabwe Mines and Minerals Development Ministry, a significant volume driven almost entirely by Chinese-owned operations. But that ore leaves Zimbabwe as spodumene concentrate, travels to China for refining into lithium carbonate or hydroxide, and then re-enters the global supply chain as a processed chemical rather than a Zimbabwean product. Zimbabwe captures mining revenue and royalties. China captures the processing margin. The battery cell manufacturer — whether in Asia, Europe, or Morocco — buys a commodity.

Whether Kenitra’s specific lithium feedstock flows through Zimbabwean deposits is not publicly confirmed. What is certain is that the value chain from Zimbabwean mine to Moroccan cell passes through China at the processing stage — a structural dependency that no African manufacturing investment changes unless the processing step moves.

The DRC Cobalt Question — and Why It Is Partly the Wrong Question

The Democratic Republic of Congo supplied approximately 73 per cent of global cobalt production in 2024, according to the USGS. For nickel-manganese-cobalt (NMC) battery chemistries — the dominant technology in premium EVs and consumer electronics — DRC cobalt is structurally indispensable. The same Chinese firms active in Zimbabwe’s lithium sector are deeply embedded in DRC’s cobalt mines: CMOC Group (formerly China Molybdenum), Zijin Mining, and the trading operations of Trafigura and Glencore all extract and process Congolese cobalt for global battery supply chains.

But Gotion’s Kenitra factory complicates the DRC narrative in a specific way. LFP batteries contain no cobalt. The Gotion facility is an LFP plant. For this investment, DRC cobalt is irrelevant — not because the DRC’s position is secure, but because the specific chemistry deployed in Morocco has deliberately engineered cobalt out of the equation. This is not incidental: LFP chemistry has been gaining market share against NMC precisely because it eliminates the cobalt supply concentration risk, and Chinese manufacturers including CATL and Gotion have led that shift partly to reduce their dependence on Congolese supply chains that are politically volatile and subject to export restriction risk.

The DRC faces a more complex challenge than whether a Moroccan factory uses its cobalt. The real structural question is whether, as the battery industry progressively moves toward lower-cobalt or cobalt-free chemistries, the DRC’s exceptional mineral endowment translates into less leverage rather than more. The Natural Resource Governance Institute’s 2025 Africa Mining Report noted that the DRC government has been intensifying discussions around downstream processing requirements in its mining code — but implementation remains limited by power infrastructure constraints that make energy-intensive smelting and refining operations economically marginal outside of Chinese-funded special economic zones.

Why Morocco Won — and What the Others Lack

The investment case for Kenitra is not primarily about minerals. Morocco’s structural advantages over DRC, Zimbabwe, and Zambia as a battery manufacturing location are almost entirely about everything except what is in the ground.

The Morocco-EU Association Agreement, in force since 2000 and progressively deepened, gives Moroccan industrial exports tariff-free access to European markets — a decisive advantage as the EU’s Carbon Border Adjustment Mechanism and battery supply chain regulations create strong incentives for European automakers to source locally-adjacent rather than Asia-sourced battery inputs. Kenitra’s proximity to Stellantis and Renault’s existing Moroccan assembly operations means Gotion is supplying a customer already on-site. The Atlantic Free Zone offers investor-grade legal infrastructure, a single administrative window for permits and licenses, and logistics connections to European ports that DRC’s landlocked mining provinces cannot match.

Power supply is the most fundamental constraint. Industrial-scale battery cell manufacturing requires continuous, reliable, high-voltage electricity. Morocco’s grid, while carbon-intensive, is stable. The ACWA Power renewable energy partnership addresses the sustainability dimension. By contrast, the DRC — despite holding the Congo River hydroelectric potential to power significant portions of sub-Saharan Africa — has a transmission infrastructure so underdeveloped that Kinshasa experiences regular blackouts. Zambia’s copper belt provinces are better served but still face grid reliability constraints that raise manufacturing risk premiums. Zimbabwe’s power deficit has been a structural drag on industrial investment for over a decade.

Political risk pricing completes the calculation. Multilateral lenders and development finance institutions apply risk-adjusted cost of capital to industrial investments that reflects country risk, regulatory predictability, and expropriation risk. Morocco is rated investment grade by all three major ratings agencies. DRC, Zimbabwe, and Zambia are not. A $5.6 billion greenfield manufacturing investment requires long-term financing at rates that investment-grade sovereign environments enable and sub-investment-grade environments make prohibitive.

What the Mineral-Rich Countries Would Actually Need

Zimbabwe’s government read this gap correctly, if incompletely, when it banned the export of raw lithium ore and unprocessed spodumene concentrate in 2023. The policy rationale was sound: without processing requirements, the country functions as a quarry for Chinese manufacturers who capture the value-added steps. The implementation challenge is that banning exports without the infrastructure to process domestically simply reduces investment flows without building industrial capacity.

What Zimbabwe, Zambia, and DRC would need to replicate the Kenitra model — or more precisely, to build a version of it anchored in their actual mineral endowments — is a convergence of investments that none of them has yet achieved simultaneously: transmission infrastructure capable of supporting energy-intensive manufacturing; a bilateral trade agreement with a high-income market that creates downstream demand; a domestic or regional industrial cluster large enough to anchor supply chain investment; and a sovereign risk profile that enables long-tenor manufacturing finance at competitive rates.

Morocco spent a decade building those conditions before Gotion arrived. The Stellantis and Renault investments preceded the gigafactory by years; the renewable energy infrastructure preceded the battery plant; the free zone legal framework preceded the Chinese investor. The lesson of Kenitra is not that mineral endowment is irrelevant — Morocco’s phosphate reserves are genuinely significant for LFP — but that mineral endowment is necessary and far from sufficient.

The Window Is Not Permanent

The battery manufacturing investment wave is moving fast. CATL, BYD, Samsung SDI, and LG Energy Solution are all evaluating or executing European and North African manufacturing expansions driven by the same EU regulatory pressure that attracted Gotion to Morocco. Each facility that gets built represents a supply chain commitment measured in decades, not years.

For DRC, Zimbabwe, and Zambia, the window to insert themselves into the manufacturing tier of the battery supply chain — rather than remaining at the extraction tier — is open now and will begin closing as European and North African manufacturing capacity comes online. The infrastructure gaps, governance constraints, and financing disadvantages that explain why Morocco won the first gigafactory are not immutable. But they require the kind of sustained, co-ordinated investment in grid infrastructure, trade relationships, and institutional development that has not yet been prioritised by any of the three mineral-rich countries at the scale the moment requires.

Africa has the battery minerals. Morocco is building the first battery factory. Whether that asymmetry persists through the next decade of energy transition investment depends on decisions being made now — in Kinshasa, Harare, and Lusaka, as much as in Kenitra.