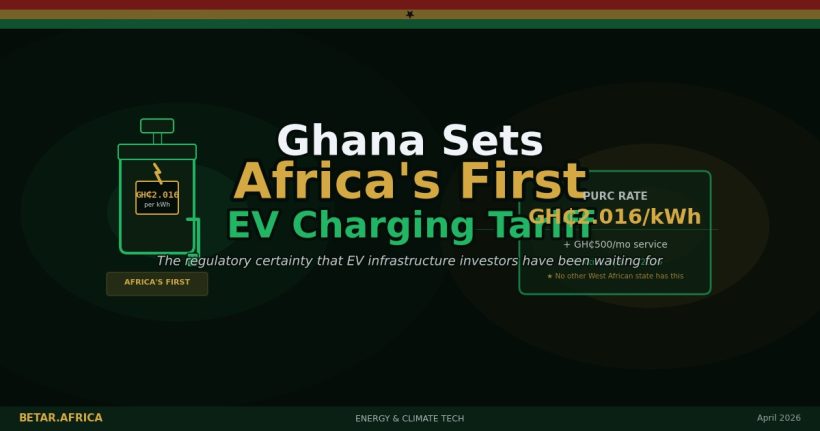

Ghana Just Did What No West African Country Has Done: Put a Price on Charging an EV

Buried inside a routine quarterly electricity tariff review was something historically significant: Africa’s first regulated commercial EV charging rate. Ghana’s PURC set it at GH₵2.016 per kilowatt-hour. That number matters less than the fact that it exists at all.

On March 13, 2026, Ghana’s Public Utilities Regulatory Commission announced its quarterly electricity tariff revision. The headline was a 4.81% reduction in standard consumer electricity bills, effective April 1. Macroeconomic conditions drove the decision: the cedi had appreciated 6.78% against the dollar between quarterly reviews, and three-month average inflation had fallen to 4.17% — well below the 8% assumption built into the previous quarter’s rates. Industrial users received even sharper relief, with cuts of up to 15.43%.

The press coverage treated it as a monetary policy dividend story. That framing was correct but incomplete. Embedded at the bottom of the same regulatory decision was something that has nothing to do with macroeconomic conditions and everything to do with what kind of economy Ghana is positioning itself to become: Africa’s first regulated commercial EV charging tariff.

The rate: GH₵2.016 per kilowatt-hour, plus a GH₵500 per month service charge. No other West African country — not Nigeria, not Senegal, not Côte d’Ivoire, not Cameroon — has issued an equivalent.

The Business Model Question It Answers

For the past three years, the same conversation has repeated itself in every EV infrastructure investment meeting across West Africa: what is the business model? An investor willing to deploy capital into public EV charging stations needs to know what rate they can charge end users for electricity. Without a regulated tariff, the answer has been: whatever you can negotiate with the grid operator, subject to revision without notice, and legally ambiguous in any case.

That uncertainty is not a minor friction. It is the foundational barrier to financing. A 50kW DC fast charger in an African market — once grid backup costs are included — runs between $65,000 and $90,000 installed. That capital cannot be committed without a revenue model, and a revenue model cannot exist without a price. Ghana just provided the price.

This is what makes the PURC decision structurally significant beyond its numbers. The question EV infrastructure investors have been asking is not “what is the rate?” — it is “does a rate exist at all?” Ghana has answered in the affirmative. Investors can now model returns, structure debt, and approach development finance institutions with a project that has a defined revenue line. The regulatory certainty is the product, not the specific rate.

Policy Ahead of Adoption

Ghana’s EV market is small. The country has an estimated 17,000 electric vehicles in use, the majority of them electric tricycles and imported two-wheelers. Public charging infrastructure is nearly non-existent — fewer than 12 public chargers serve a country of 33 million people. By comparison, Africa as a whole has fewer than 200 public EV chargers against Europe’s Netherlands alone operating 150,000.

That makes the PURC decision a deliberate act of sequencing, not a reactive policy response. Ghana is setting the regulatory architecture before the demand arrives — which is the opposite of how most infrastructure regulation in Africa has worked historically. Typically, regulation follows adoption, which means investors wait, adoption stalls for lack of infrastructure, and the market never reaches the volume needed to trigger the regulation in the first place.

The PURC tariff fits into a broader policy stack that Ghana has been quietly assembling. The Energy Commission issued updated EV regulatory guidelines in February 2026. Import duty waivers on electric vehicles have been extended through 2027. The government’s EV adoption target — 70% of new vehicle registrations electric by 2045, with full internal combustion engine phase-out by 2070 — requires charging infrastructure to be in place years before the target dates. The tariff is the missing regulatory layer that enables private capital to begin building that infrastructure now.

The Rate Debate

Not everyone in Ghana’s energy sector considers the GH₵2.016/kWh rate well-designed. The Association for the Study of the Economy and Communities has called for “adjustments to ensure inclusive growth,” proposing a tiered structure that would differentiate pricing based on consumption volume and geographic location. Under the ASEC proposal, operators below a 500kWh/month threshold — primarily small operators in rural or peri-urban areas — would receive a more favourable rate than high-volume urban charging stations.

The concern is that a flat national rate, priced for commercial viability in Accra, will concentrate investment in urban centres and leave Ghana’s secondary cities without the charging infrastructure required to support EV adoption beyond the capital. It is a legitimate critique. Ghana’s domestic EV industry — including Kantanka Automobile Company, which produces electric vehicles in Ghana — is also watching how the rate structure evolves, given that domestic manufacturers’ commercial viability depends partly on whether Ghanaian consumers can charge affordably outside major cities.

The PURC framework allows for rate adjustments in subsequent quarterly reviews. The first revision cycle will determine whether Ghana’s regulator is responsive to the investment signals that the initial tariff generates — or whether the rate becomes fixed in political amber.

What Ghana Just Showed the Rest of West Africa

The deepest significance of the PURC decision is not what it does for Ghana’s EV market in 2026. It is what it demonstrates is possible across the region.

Ghana did not need new legislation to create an EV charging tariff. It did not need a dedicated EV infrastructure law, a presidential executive order, or a parliamentary vote. It needed a quarterly tariff review — the same administrative process that adjusts electricity prices for industrial and residential consumers every three months — and the regulatory will to include a new tariff category within it. The mechanism already existed. Ghana used it.

Nigeria, Senegal, Côte d’Ivoire, and Cameroon all have electricity sector regulators with similar quarterly review processes. None have issued commercial EV charging rates. The institutional infrastructure to replicate Ghana’s decision exists in every major West African market. What has been lacking is the signal that it should be done.

Ghana has now provided that signal. The question is whether West Africa’s other energy regulators are paying attention.

This article is part of BETAR.africa’s Energy & Climate Tech coverage. Related: Africa’s EV Charging Infrastructure Gap: A $5B Market, 200 Public Chargers, and the Structural Crisis No One Is Solving (BETA-773)